Highlights

- Fixed Deposits require lump-sum investment, while Recurring Deposits build savings monthly

- Interest structure differs as FD earns on full amount, RD earns on incremental deposits

- Choice depends on income pattern, savings discipline, and financial goals

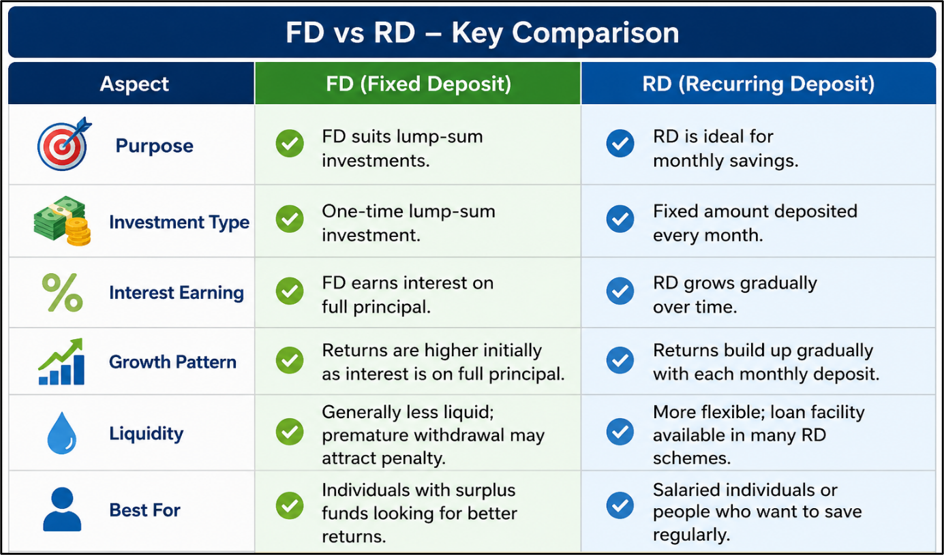

Fixed Deposits (FDs) and Recurring Deposits (RDs) remain among the most widely used savings instruments in India. Both are offered by banks and financial institutions and are considered low-risk options with predictable returns. However, despite their similarities in safety and structure, they serve different financial needs and saving behaviours.

FDs are generally used when an individual has a lump sum amount to invest for a fixed tenure, while RDs are designed for disciplined monthly savings over a chosen period. Understanding the difference between the two helps in aligning investment decisions with financial goals.

Source: Analysis by Kalkine

How Fixed Deposits Work

A Fixed Deposit allows an investor to place a one-time lump sum amount with a bank for a specific tenure at a predetermined interest rate. The interest rate remains fixed throughout the investment period, and the maturity amount is paid at the end of the tenure or at regular intervals depending on the chosen payout option.

Since the entire principal is invested at once, the interest calculation begins on the full amount from the start. This structure makes FD suitable for individuals who already have savings and prefer predictable returns over a fixed period.

How Recurring Deposits Work

A Recurring Deposit allows individuals to invest a fixed amount every month for a pre-decided tenure. Each monthly installment is treated as a separate deposit, and interest is calculated accordingly.

This structure supports regular savings habits, especially for salaried individuals who prefer building a corpus gradually. The maturity amount includes all monthly contributions along with accumulated interest earned over time.

Key Differences Between FD and RD

The primary difference lies in the mode of investment. FD requires a single lump sum, while RD requires periodic monthly contributions. Because FD invests the entire amount at once, it generally earns higher interest compared to RD for the same tenure and rate.

In contrast, RD spreads the investment over time, which means the average amount earning interest is lower in the initial phase. This makes RD more suitable for individuals who do not have a large initial corpus but want to build savings steadily.

Interest Calculation and Returns

In FD, interest is calculated on the full principal amount from the beginning of the tenure, which allows compounding to work on a larger base. In RD, each monthly deposit earns interest only after it is added, leading to a gradually increasing investment base.

As a result, FD maturity value is often higher when compared to RD with similar monthly savings capacity, assuming the same tenure and interest rate conditions.

Withdrawal and Flexibility

Both FD and RD allow premature withdrawal in most cases, but penalties may apply. FD withdrawals typically result in reduced interest rates, while RD withdrawals may lead to loss of interest benefits on incomplete tenure.

Flexibility depends on the bank’s terms, but both instruments are generally designed for medium-term savings discipline rather than frequent liquidity needs.

Taxation Aspect

Interest earned from both FD and RD is taxable under the Income Tax Act. Banks may also deduct tax at source if interest exceeds the prescribed threshold. Tax treatment remains similar for both instruments, with no major structural difference in taxation.

Risks to Watch

- Premature withdrawal may reduce overall interest earnings

- Inflation can reduce real returns over long periods

- Interest income is fully taxable, reducing net returns

- Lower liquidity compared to savings accounts during tenure

Summary

Fixed Deposits and Recurring Deposits are both low-risk savings tools but serve different purposes. FDs are suitable for lump-sum investments where funds are already available, while RDs help build savings through monthly contributions. The main differences lie in deposit structure, interest accumulation, and savings discipline. Choosing between them depends on income flow, financial goals, and liquidity needs.

FAQs

Q: What is the main difference between FD and RD?

A: FD requires a lump sum investment, while RD requires fixed monthly contributions over a chosen tenure.

Q: Which gives higher returns, FD or RD?

A: FD generally gives higher returns because the full amount earns interest from the beginning of the tenure.

Q: Can FD and RD be withdrawn before maturity?

A: Yes, both allow premature withdrawal, but penalties and reduced interest may apply depending on bank rules.