Highlights

- Several categories of income remain exempt under provisions of the Income Tax Act.

- Tax-free income may still need disclosure while filing income tax returns.

- Eligibility conditions and limits determine whether exemptions remain available.

While most taxpayers focus on deductions and rebates during tax filing season, exempt income can be equally important from a compliance perspective. Indian tax laws provide exemptions for certain categories of income, helping taxpayers reduce their overall tax burden when specific conditions are met.

Tax professionals note that exempt income should still be disclosed appropriately in income tax returns, even when no tax is payable. With updated return forms requiring more detailed disclosures, understanding these exemptions has become increasingly important for taxpayers preparing returns for Assessment Year 2026-27.

Source: Analysis by Kalkine

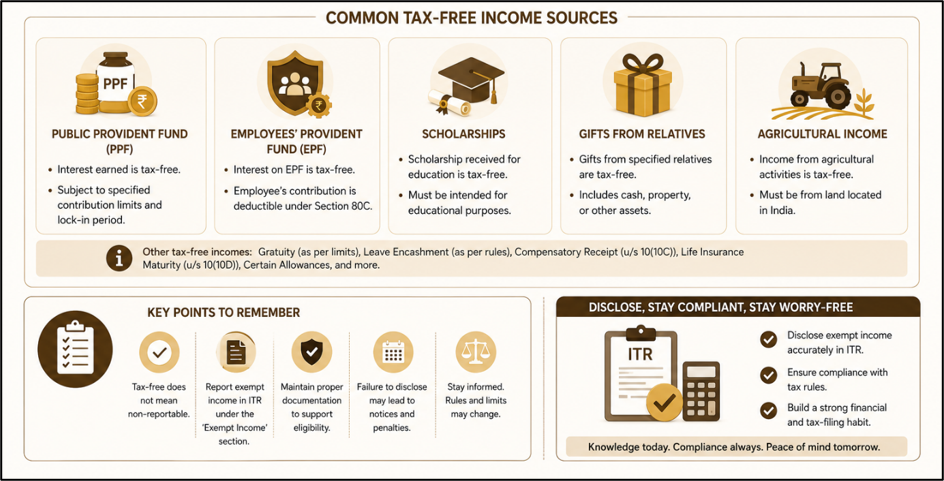

Agricultural Income Continues to Remain Outside the Tax Net

Income generated from agricultural activities conducted on land situated in India generally qualifies for exemption under the Income Tax Act. This includes earnings from cultivation, agricultural operations, and revenue derived from agricultural land.

The provision reflects the long-standing policy of keeping qualifying farm income outside the scope of income taxation.

HUF Distributions Receive Separate Treatment

Members receiving money from a Hindu Undivided Family (HUF) may not face taxation on such receipts when the distribution is made from income already taxed at the HUF level.

Since the HUF is treated as a separate taxable entity, distributions to members are generally not taxed again in their hands, preventing double taxation of the same income.

Partnership Profit Shares Are Generally Exempt

Partners in partnership firms and Limited Liability Partnerships (LLPs) may receive a share of profits that is exempt from tax in their individual hands.

However, this exemption typically applies only to the profit share. Interest on capital, remuneration, commission, or other payments received from the firm may continue to be taxable according to applicable provisions.

Gifts and Inherited Assets

Tax rules provide relief for gifts received from specified relatives. Such receipts are generally exempt regardless of value, provided they fall within the prescribed definition of relatives under tax laws.

Similarly, assets inherited through succession or received following the death of an individual are generally not taxed as income in the hands of legal heirs. Certain gifts received on the occasion of marriage may also qualify for exemption.

Educational Scholarships Remain Tax-Free

Scholarships awarded to support educational expenses generally enjoy tax-exempt status.

The objective is to ensure that financial assistance provided for education is used for academic purposes without creating an additional tax burden for students and their families.

Retirement Benefits Can Receive Exemptions

Gratuity received upon retirement may qualify for tax exemption, subject to applicable conditions and limits.

Government employees generally enjoy broader exemptions, while non-government employees can claim benefits within prescribed ceilings. Leave encashment received at retirement may also qualify for tax relief, depending on eligibility and applicable limits.

Tax-Advantaged Savings Schemes

Several government-backed savings schemes offer tax-free interest and maturity benefits when conditions are satisfied.

These may include:

- Public Provident Fund (PPF)

- Employees' Provident Fund (EPF)

- Voluntary Provident Fund (VPF)

- Sukanya Samriddhi Yojana (SSY)

The exemption typically depends on compliance with scheme rules, tenure requirements, and withdrawal conditions.

Provident Fund Withdrawals

Withdrawals from recognised provident fund accounts may remain tax-free when statutory conditions are fulfilled.

Generally, tax benefits apply when the employee completes the prescribed continuous service period or qualifies under specific exceptions recognised by tax regulations.

Life Insurance Maturity Proceeds

Amounts received on maturity of eligible life insurance policies may qualify for tax exemption, including applicable bonus components.

However, the exemption remains subject to premium-related conditions and other requirements specified under tax law. Certain high-premium policies may not qualify for the exemption available to traditional policies.

Why Reporting Exempt Income Matters

A common misconception is that tax-free income does not need to be disclosed in income tax returns.

Tax experts indicate that exempt income should generally be reported under the appropriate schedules where required. Accurate disclosure can help avoid reporting mismatches and improve overall compliance during return processing.

Key Risks

- Incorrect exemption claims may attract tax scrutiny.

- Missing disclosures can create return mismatches.

- Certain exemptions apply only under specific conditions.

- Premature withdrawals may affect tax benefits.

Summary

Indian tax laws provide exemptions for several income categories, including agricultural income, HUF distributions, partnership profit shares, scholarships, gifts from specified relatives, provident fund withdrawals, and eligible insurance proceeds. However, many exemptions are subject to conditions, thresholds, and documentation requirements. Taxpayers should review eligibility carefully and ensure exempt income is disclosed appropriately while filing returns for AY 2026-27.

FAQs

Q: Is tax-free income required to be disclosed in an income tax return?

A: In many cases, exempt income should still be reported in applicable return schedules.

Q: Are gifts from family members taxable in India?

A: Gifts from specified relatives are generally exempt, subject to applicable tax provisions.

Q: Can life insurance maturity proceeds be tax-free?

A: Yes, eligible policies may qualify for exemption if prescribed conditions are satisfied.