Highlights

- Stamp duty and registration fees can significantly raise the total cost of purchasing a home.

- These charges are generally paid upfront and are not covered by most home loans.

- Ignoring transaction-related expenses may lead to budget overruns during property purchases.

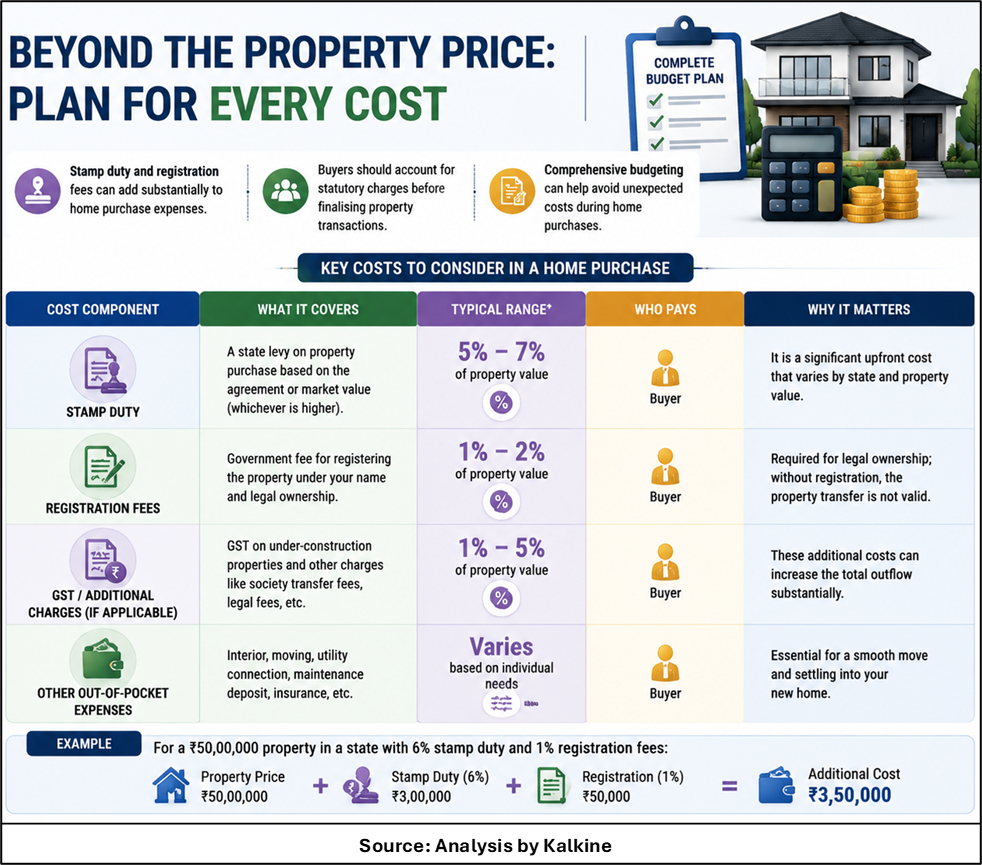

For many homebuyers, the focus remains on the property's advertised price, down payment requirements, and monthly loan instalments. However, the actual cost of buying a home extends beyond these figures. Stamp duty and registration charges are mandatory expenses that can add a substantial amount to the total acquisition cost. These charges are often overlooked during the budgeting process, creating financial pressure when the transaction nears completion.

Understanding Stamp Duty And Registration Charges

Stamp duty is a tax imposed by state governments on property transactions, while registration charges are paid to legally record the ownership transfer. Both are essential for establishing legal ownership of a property. The amount payable varies across states and may depend on factors such as property value, location, property type, and buyer category.

Why These Charges Affect Home Budgets

Many buyers calculate affordability based on the property's sale price and expected loan eligibility. However, lenders typically finance only the property cost and do not cover stamp duty or registration fees. As a result, buyers must arrange these funds separately. This can strain savings, particularly for first-time buyers who have already allocated funds toward the down payment.

The Need For A Wider Cost Assessment

Stamp duty and registration expenses are only part of the overall transaction cost. Buyers may also encounter loan processing fees, legal verification expenses, maintenance deposits, parking charges, utility connection fees, and interior furnishing costs. Factoring in these expenses before finalising a purchase can help prevent unexpected financial burdens later.

State-Level Variations Matter

Property-related taxes and registration fees differ across states. In some regions, concessions may be available for specific buyer categories, including women homebuyers. Because rates vary significantly, prospective buyers should verify applicable charges in their state before making financial commitments.

Budgeting For The Full Purchase Cost

Financial planners often recommend maintaining a separate buffer for transaction-related expenses. Considering only the property's listed value can create an incomplete picture of affordability. A comprehensive budget should include statutory charges, financing costs, furnishing expenses, and emergency reserves to avoid last-minute borrowing. Community discussions among homebuyers frequently highlight stamp duty, registration fees, maintenance deposits, and legal charges as costs that are commonly underestimated.

Can Buyers Receive Tax Benefits?

Under current tax provisions, stamp duty and registration charges may qualify for deduction under Section 80C, subject to applicable conditions and limits. Buyers should review eligibility requirements and consult tax professionals before claiming deductions.

Key Risks

- Underestimating upfront statutory charges can disrupt purchase plans.

- Home loans generally do not cover stamp duty and registration fees.

- Additional transaction expenses can exceed initial estimates.

- Insufficient liquidity may require unplanned borrowing.

Summary

The listed price of a property is only one component of home ownership costs. Stamp duty, registration charges, and other transaction-related expenses can materially increase the amount buyers need to arrange. Evaluating the complete financial commitment before signing an agreement can help buyers avoid budget shortfalls and make more informed property purchase decisions.

FAQs

Q: What are stamp duty and registration charges?

A: They are mandatory government charges required to legally transfer property ownership to a buyer.

Q: Are stamp duty and registration fees included in home loans?

A: In most cases, lenders do not finance these charges, requiring separate payment by buyers.

Q: Why should buyers budget beyond the property price?

A: Additional expenses such as taxes, fees, interiors, and maintenance deposits can significantly increase costs.