Highlights

- Asset allocation between equity and debt typically changes with age and financial goals.

- Younger investors may allocate more to equity due to a longer investment horizon.

- Debt allocation generally rises closer to retirement to help manage portfolio volatility.

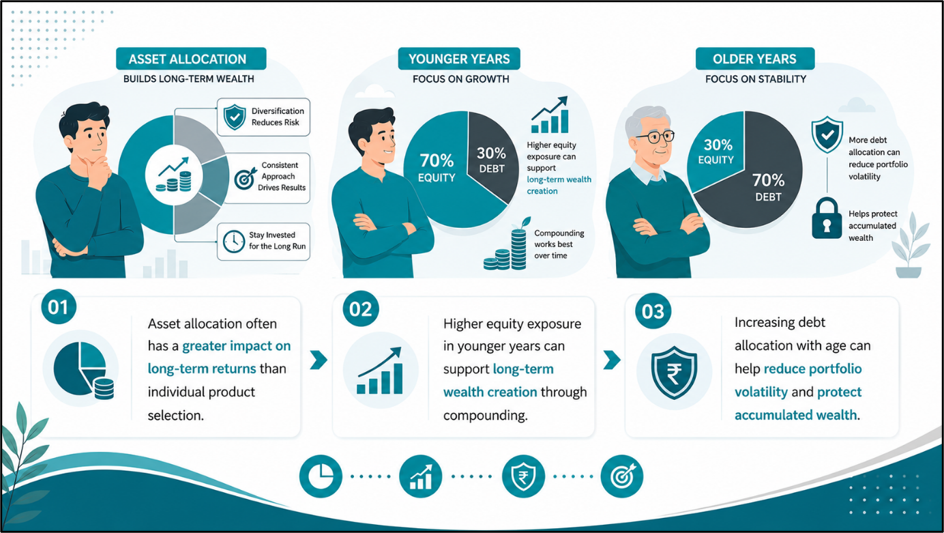

When it comes to investing, many individuals spend considerable time selecting stocks, mutual funds or fixed-income products. However, financial experts often view asset allocation—the mix of equity and debt in a portfolio—as one of the most important factors influencing long-term investment outcomes.

Asset allocation helps balance growth potential and risk. Equity investments offer the potential for higher long-term returns but can experience significant market fluctuations. Debt investments, on the other hand, generally provide greater stability and predictable income, although they may offer lower return potential over extended periods.

The right mix between these two asset classes often depends on an investor's age, financial goals and risk tolerance.

Source: Analysis by Kalkine

The Logic Behind Age-Based Investing

One widely used principle in financial planning is that asset allocation should evolve as investors move through different life stages. Younger individuals typically have more time to recover from market downturns and may therefore be able to take greater exposure to equity.

As retirement approaches, preserving accumulated wealth often becomes increasingly important. Consequently, many investors gradually increase their allocation to debt instruments to reduce portfolio volatility and protect capital.

While age is an important consideration, factors such as income stability, financial responsibilities and investment objectives should also influence allocation decisions.

In Your 20s: Focus on Long-Term Growth

Investors in their twenties generally have the longest investment horizon. With retirement potentially several decades away, they may be in a position to withstand short-term market fluctuations in pursuit of long-term wealth creation.

A portfolio allocation of around 80% to 90% in equity and 10% to 20% in debt is often considered suitable for investors in this age group, depending on individual risk appetite. The higher equity allocation allows investors to benefit from long-term compounding and potential market growth.

Debt investments can still play a role by providing liquidity and helping meet short-term financial goals.

In Your 30s: Balancing Growth and Responsibilities

As individuals enter their thirties, financial responsibilities often increase. Home loans, family expenses and children's education planning may begin to influence investment decisions.

At this stage, an allocation of approximately 70% to 80% in equity and 20% to 30% in debt may help balance growth objectives with risk management. Investors can continue focusing on long-term wealth creation while gradually building stability into their portfolios.

Regular portfolio reviews become increasingly important during this phase to ensure investments remain aligned with changing financial goals.

In Your 40s: Increasing Stability

By the time investors reach their forties, retirement planning generally becomes a more prominent objective. While growth remains important, protecting accumulated wealth may begin to receive greater attention.

Many financial planners suggest considering a portfolio allocation of around 60% to 70% in equity and 30% to 40% in debt during this stage. This approach allows investors to participate in potential market gains while reducing exposure to significant market volatility.

The exact allocation should reflect individual circumstances, including retirement timelines and income stability.

In Your 50s: Preparing for Retirement

Investors in their fifties are often approaching retirement and may have a shorter time horizon for recovering from major market declines.

A portfolio allocation of approximately 40% to 60% in equity and 40% to 60% in debt may help strike a balance between growth and capital preservation. The increased debt exposure can provide greater stability and reduce the impact of market fluctuations on retirement savings.

However, investors with longer working careers or higher risk tolerance may choose a different allocation based on their specific needs.

Post-Retirement: Focus on Capital Preservation

After retirement, the primary objective often shifts from wealth accumulation to income generation and capital preservation.

Many retirees consider maintaining a larger allocation to debt instruments, with equity exposure retained to support long-term portfolio growth and help combat inflation. The exact mix depends on income requirements, healthcare needs and overall financial resources.

A diversified approach can help retirees manage both longevity risk and market risk.

Why Rebalancing Is Important

Asset allocation is not a one-time exercise. Market movements can cause portfolios to drift away from their intended allocation over time.

Periodic rebalancing helps restore the desired mix between equity and debt. This process can help investors maintain an appropriate risk profile and ensure that their portfolios remain aligned with long-term financial objectives.

Reviewing allocations annually or after major life events can support more effective portfolio management.

Key Risks to Watch

- Excessive equity exposure can increase portfolio volatility.

- Overreliance on debt may limit long-term wealth creation.

- Ignoring asset allocation can distort portfolio risk levels.

- Failure to rebalance may affect investment objectives.

Summary

Asset allocation between equity and debt plays a critical role in managing investment risk and return potential. Younger investors often maintain higher equity exposure to benefit from long-term growth, while debt allocation typically increases with age to provide greater stability. Although age-based guidelines can serve as a useful starting point, investors should also consider financial goals, risk tolerance and personal circumstances when determining the appropriate portfolio mix.

FAQs

Q: Why should equity allocation generally reduce with age?

A: As retirement approaches, investors often prioritise capital preservation and lower portfolio volatility over aggressive growth.

Q: Is age the only factor that determines asset allocation?

A: No. Financial goals, income stability, risk tolerance and investment horizon are also important considerations.

Q: How often should investors review their asset allocation?

A: Reviewing portfolios annually or after significant life events can help maintain alignment with financial objectives.