Highlights

- Even occasional smoking may affect health insurance underwriting decisions.

- Insurers often classify social smokers under smoker categories for risk assessment.

- Incorrect disclosure of smoking habits can create claim-related complications.

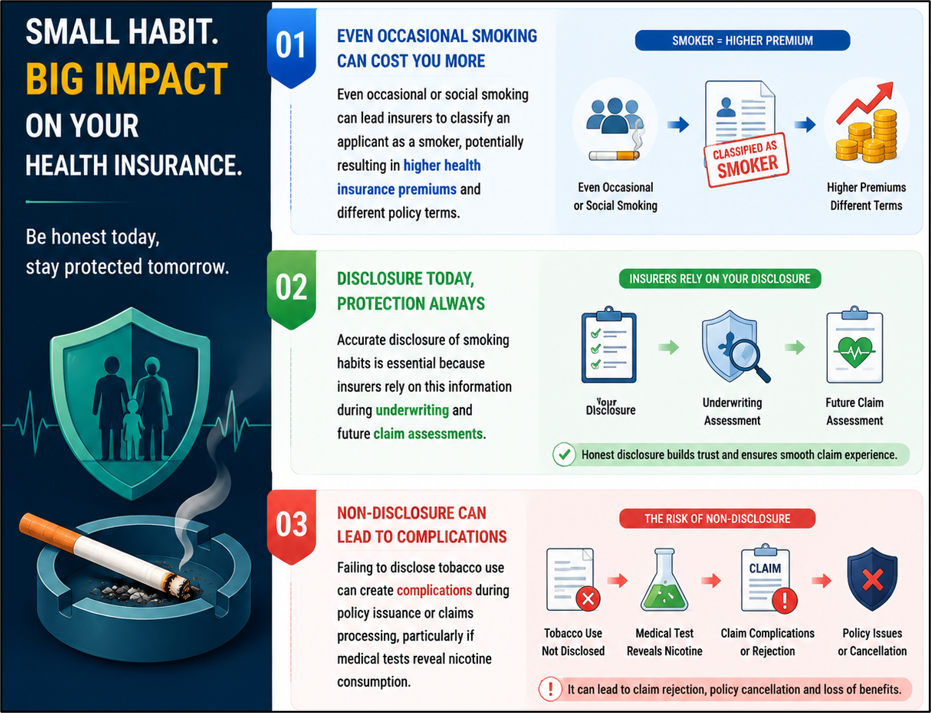

Many people who smoke only at parties, social gatherings or occasional events do not consider themselves smokers. However, health insurance companies may view the situation differently. From an insurer’s perspective, tobacco consumption—even if infrequent—can represent a higher health risk compared to a non-smoker. As a result, individuals who identify as “social smokers” may still be treated as smokers during the underwriting process, potentially affecting premiums, policy terms and eligibility.

Source: Analysis by Kalkine

Why Insurers Focus on Smoking Habits

Health insurance pricing is based on risk assessment. Insurers evaluate factors such as age, medical history, lifestyle habits and existing health conditions to estimate the likelihood of future claims. Tobacco use remains one of the most significant lifestyle risk factors because it has been linked to various health conditions, including heart disease, respiratory illnesses and certain forms of cancer.

For this reason, insurers generally seek detailed information about an applicant’s smoking habits, regardless of whether the individual smokes daily or only occasionally. The primary concern is not the frequency alone but the presence of tobacco use as a risk factor.

Social Smokers May Not Qualify as Non-Smokers

Many applicants assume that smoking only a few cigarettes during social occasions does not require disclosure. However, insurance companies often use broader definitions when classifying smokers and non-smokers. Even infrequent use of cigarettes, cigars, vaping products or other tobacco-related products may lead to classification as a smoker.

Since underwriting standards vary among insurers, definitions can differ across companies. Nevertheless, occasional tobacco consumption is often treated more cautiously than applicants expect.

Disclosure Is More Important Than Frequency

When purchasing health insurance, applicants are typically required to answer questions about tobacco and nicotine consumption. Providing accurate information is critical because insurers rely on these declarations while issuing policies.

The issue is not necessarily whether a person smokes daily or socially. Instead, insurers focus on whether the applicant has disclosed the habit honestly. Failure to provide accurate information could create difficulties later if a claim is investigated and undisclosed tobacco use is discovered.

Medical Tests Can Reveal Tobacco Consumption

In some cases, insurers may request medical examinations before issuing coverage. Certain tests can identify the presence of nicotine or tobacco-related substances in the body. Even when smoking is occasional, traces may still be detected depending on the timing and nature of the consumption.

As a result, inconsistencies between declarations and medical findings can raise additional questions during underwriting. Accurate disclosure can help avoid unnecessary complications during policy issuance.

Premiums May Differ for Smokers

Individuals classified as smokers often face higher premiums than non-smokers because insurers consider them a higher-risk category. The difference in premiums can vary depending on age, coverage amount, insurer guidelines and overall health profile.

While occasional smokers may feel that their risk level is lower than that of regular smokers, insurance pricing models generally focus on the presence of tobacco use rather than personal perceptions of smoking frequency.

Non-Disclosure Can Create Claim Challenges

One of the biggest risks associated with inaccurate declarations is the possibility of disputes during claims assessment. If an insurer determines that relevant information about tobacco use was withheld at the time of application, it may examine whether the omission affected underwriting decisions.

This does not automatically result in claim rejection in every case, but it can lead to additional scrutiny, requests for clarification and longer claim-processing timelines.

Quitting Smoking Can Improve Future Insurance Terms

Individuals who stop smoking may eventually qualify for non-smoker status, depending on insurer-specific guidelines. Many insurers require applicants to remain tobacco-free for a specified period before considering reclassification. Documentation, declarations and, in some cases, medical evidence may be required during this process.

Those planning to quit smoking may wish to review insurer requirements to understand how non-smoker status is determined.

Honesty Remains the Best Approach

Health insurance is designed to provide financial protection during medical emergencies, making transparency during the application process essential. Whether smoking is frequent or occasional, accurate disclosure allows insurers to assess risk appropriately and helps reduce the possibility of future disputes.

For social smokers, the safest approach is to review policy questions carefully and provide complete information rather than assuming occasional tobacco use will be treated as non-smoking behaviour.

Key Risks

- Social smoking may still result in smoker classification.

- Higher premiums may apply because of tobacco-related risks.

- Medical tests can reveal undisclosed nicotine consumption.

- Incorrect disclosures may complicate future claim assessments.

Summary

Occasional or social smoking may not be viewed the same way by insurers as it is by consumers. Health insurance companies often consider any tobacco use during underwriting and may classify social smokers as smokers for risk assessment purposes. Accurate disclosure of smoking habits is important because non-disclosure can create complications during policy issuance or claims processing. Understanding insurer definitions and reporting habits honestly can help policyholders avoid future issues.

FAQs

Q: Can a social smoker be treated as a smoker by health insurers?

A: Yes, many insurers consider any tobacco use when determining smoker status and premium rates.

Q: Why do insurers ask about occasional smoking habits?

A: Tobacco use is a health risk factor that can influence underwriting and pricing decisions.

Q: Can non-disclosure of smoking habits affect insurance claims?

A: Yes, inaccurate disclosures may lead to additional scrutiny during claim evaluation and processing.