Axis Bank Limited (NSE:AXISBANK) reported a mixed yet operationally resilient performance for the quarter and financial year ended March 31, 2026, as robust business growth and improving asset quality were partially offset by elevated provisioning and treasury-related pressures. The private lender posted a standalone net profit of ₹7,071 crore in Q4FY26, marginally lower than ₹7,117 crore reported in the corresponding quarter last year.

The earnings announcement triggered a cautious market reaction, with Axis Bank shares declining nearly 4–5% intraday after results amid investor concerns over higher provisions and weaker treasury income. However, several brokerages maintained constructive long-term views, citing strong advances growth and stable asset quality trends.

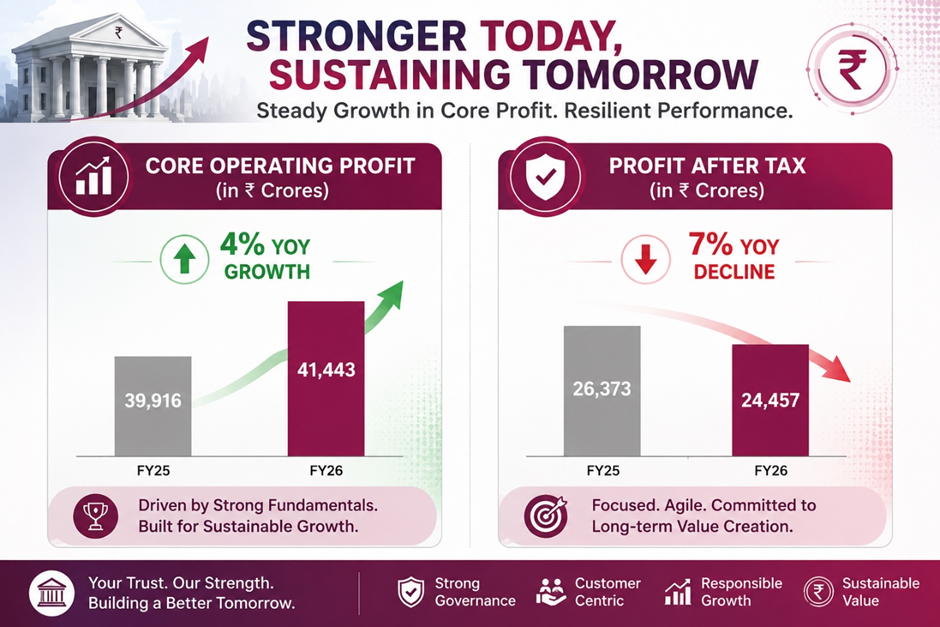

Data Source: Company Filing

Net Interest Income (NII) for Q4FY26 rose 5% year-on-year to ₹14,457 crore, while Net Interest Margin (NIM) stood at 3.62%. Fee income increased 4% YoY to ₹6,561 crore, supported by healthy growth in retail and granular fee segments. Core operating revenue improved 3% both sequentially and annually, reflecting the bank’s continued focus on diversified revenue streams.

Axis Bank’s advances grew a strong 19% YoY to ₹12.34 lakh crore, led by corporate loans, SME lending, and retail expansion. Corporate loans surged 38% YoY, SME loans increased 24%, while retail advances rose 8%. Deposits also remained healthy, growing 14% YoY to ₹13.36 lakh crore, with CASA deposits rising 11%. The CASA ratio stood at 40%, among the strongest across large private banks in India.

Asset quality metrics improved further during the quarter. Gross NPA declined to 1.23% from 1.40% in Q3FY26, while Net NPA improved to 0.37%. Gross slippages moderated to ₹4,709 crore against ₹6,007 crore in the previous quarter, reflecting improving credit quality and disciplined underwriting standards.

A key highlight of the quarter was the bank’s decision to create an additional one-time standard asset provision of ₹2,001 crore as a precautionary buffer against evolving macroeconomic and geopolitical uncertainties. Total provisions and contingencies rose to ₹3,522 crore during Q4FY26. Management clarified that the provisioning move was prudential in nature and not linked to any deterioration in the loan portfolio.

For FY26, Axis Bank reported net profit of ₹24,457 crore, down 7% YoY, while core operating profit rose 4% to ₹41,443 crore. The bank’s balance sheet expanded 17% YoY to ₹18.87 lakh crore. Capital adequacy remained comfortable, with the CET-1 ratio at 14.38% and overall CAR at 16.42%, providing sufficient growth cushion.

Strategically, the bank continued strengthening its digital ecosystem and customer engagement initiatives. During the quarter, Axis Bank expanded partnerships with Tesla India and IndiGo, enhanced digital security through its Safety Centre and SMS Shield initiatives, and reinforced its leadership in UPI payments with nearly 36% market share.

Technical Summary

Axis Bank shares closed near ₹1,292, trading around the 50-day SMA of ₹1,297, indicating consolidation after recent volatility. The RSI near 48 suggests neutral momentum with mild weakness. Immediate support is visible around ₹1,260–1,240, while resistance is placed near ₹1,350 and ₹1,400 levels. Trend structure remains cautiously positive above long-term averages.

Chart by TradingView

Conclusion

Axis Bank delivered steady operational growth in Q4FY26 despite higher provisions impacting headline profitability. Strong advances growth, stable margins, improving asset quality, and healthy capitalization continue supporting the bank’s medium-term outlook. While near-term sentiment remains cautious, the lender’s diversified franchise and digital leadership position it well for sustainable growth ahead.

FAQs

- What was Axis Bank’s Q4FY26 net profit?

Axis Bank reported Q4FY26 standalone net profit of ₹7,071 crore, marginally down 0.6% year-on-year due to higher provisions.

- Why did Axis Bank shares fall after Q4FY26 results?

The stock declined due to elevated provisions, weaker treasury income, and investor concerns over precautionary macro-risk provisioning despite stable fundamentals.

- How was Axis Bank’s asset quality in Q4FY26?

Asset quality improved significantly with Gross NPA at 1.23% and Net NPA at 0.37%, supported by lower slippages.