India's stock market has produced several multibaggers over the past decade, but few have delivered returns as extraordinary as Cupid Limited. The healthcare and consumer products company has transformed from a niche condom manufacturer into a diversified global healthcare and FMCG player, rewarding investors with a staggering 8,215% return over the last five years, while surging nearly 884% in the past year alone.

The stock recently touched a fresh 52-week high of ₹182.50, reflecting growing investor confidence in its export-led growth model, FMCG expansion strategy, and record financial performance. With management now targeting ₹600 crore revenue and ₹180 crore net profit in FY27, investors are increasingly asking whether Cupid's growth story is only getting started.

A Multibagger Journey That Turned ₹1 Lakh into More Than ₹83 Lakhs

Cupid's stock has emerged as one of the standout performers in the small-cap healthcare segment.

An investment of ₹1 lakh made five years ago would now be worth approximately ₹83 lakh, excluding transaction costs and taxes.

The rally has been supported by improving fundamentals, expanding margins, rising exports, and the successful diversification into consumer healthcare and FMCG products.

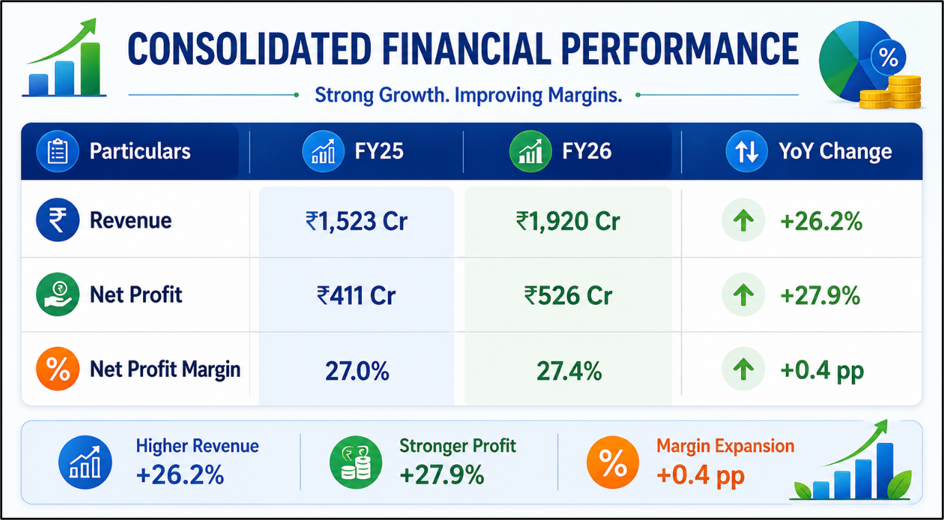

FY26: A Historic Year for Cupid

FY26 marked the strongest year in Cupid's history as the company surpassed its own guidance and delivered record revenue and profitability. Management reported revenue of ₹358 crore and net profit of ₹108 crore, exceeding its FY26 guidance of ₹335 crore revenue and ₹100 crore profit.

The company delivered growth through exports, institutional business, diagnostics, and newly launched FMCG products. Management described FY26 as the strongest quarterly and annual performance in Cupid's history.

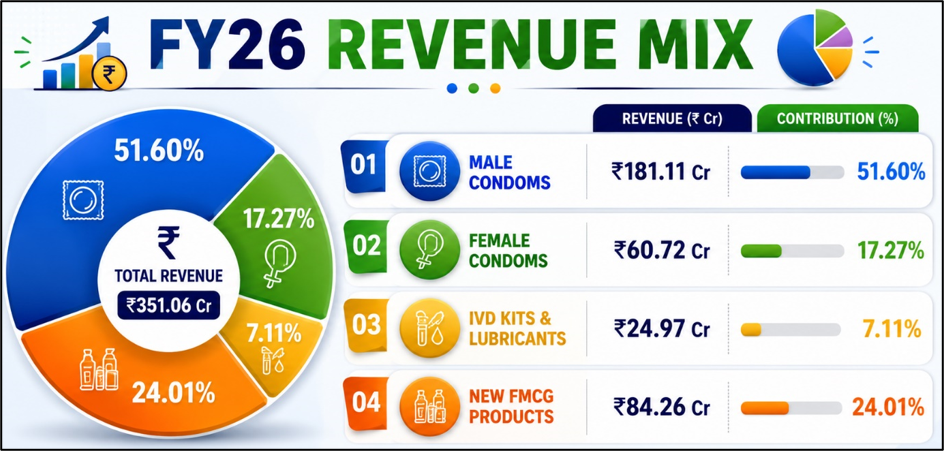

Strong Revenue Diversification Reduces Dependence on Single Product

Cupid's business model has evolved significantly beyond its traditional condom manufacturing operations.

The increasing contribution from FMCG products demonstrates the company's successful transition toward a balanced B2B and B2C business model.

FMCG Expansion Could Become the Next Growth Engine

One of the biggest developments during FY26 was Cupid's strategic investment in Baazar Style Retail.

The company announced a planned investment of ₹331.53 crore in Baazar Style Retail, with the first phase of ₹82.88 crore already deployed. The partnership gives Cupid access to more than 260 stores immediately, with the network expected to expand beyond 500 stores over the next two to three years.

Management expects this ecosystem to generate:

- ₹150 crore incremental revenue in FY27

- Up to ₹500 crore annual business potential over the medium term

- Stronger brand visibility and consumer reach

- Faster rollout of personal care and wellness products

Export Business Continues to Drive Growth

Cupid remains one of the leading global suppliers of male and female condoms, exporting products to over 125 countries and working with international organizations including WHO, UNFPA, Global Fund, PSI, and IDA Foundation.

Exports contributed ₹208.13 crore, representing approximately 59.3% of FY26 revenue, highlighting the company's strong international footprint.

The company also received CE EU IVDR certifications for HIV, Hepatitis B, Syphilis, and Pregnancy test kits, opening access to regulated European markets and strengthening its diagnostics business.

Unique Manufacturing Advantage

Cupid recently commenced development of nitrile female condoms, a premium segment traditionally dominated by a single global supplier.

The company claims to be the only manufacturer in India with integrated dual-polymer capability, allowing production of both latex and nitrile condoms. Its planned annual manufacturing capacity includes:

- ~1.25 billion male condoms

- ~125 million female condoms annually

Nitrile products typically command 25%–35% higher pricing, potentially supporting future margin expansion.

Promoter Confidence Adds Positive Signal

In June 2026, Chairman and Managing Director Aditya Kumar Halwasiya acquired 21 lakh shares from the open market, increasing promoter holding from 46.08% to 46.24%. Such promoter buying is often viewed positively by investors as it reflects confidence in the company's future prospects.

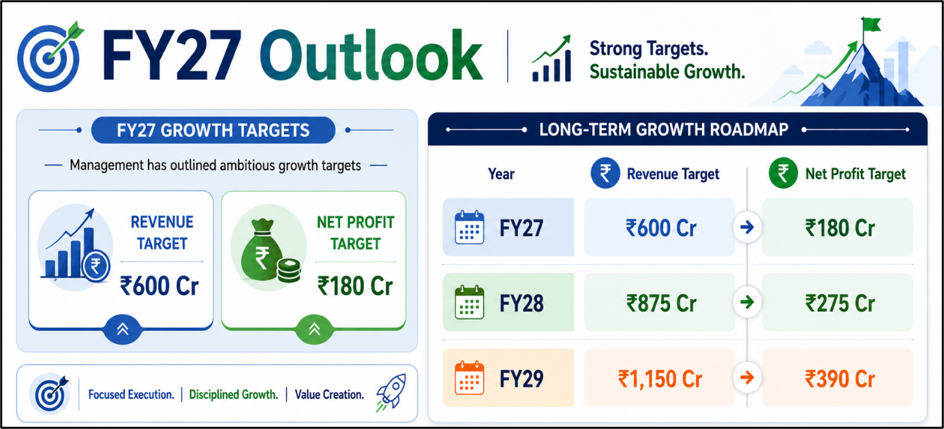

FY27 Outlook

Management has outlined ambitious growth targets:

Conclusion

Cupid Limited's transformation from a niche healthcare exporter into a diversified healthcare and FMCG company has translated into extraordinary shareholder returns. Record FY26 earnings, expanding global presence, strategic retail partnerships, premium product innovation, and promoter buying have strengthened the investment narrative.

While valuation levels have risen sharply following the stock's multibagger run, the company's strong growth visibility and ambitious FY27 targets suggest investors will continue to closely monitor whether Cupid can sustain its remarkable growth trajectory.

Frequently Asked Questions (FAQs)

- Why has Cupid Ltd become a multibagger stock?

The company delivered strong earnings growth, expanded exports, diversified into FMCG products, strengthened its retail presence, and improved profitability, resulting in substantial investor interest.

- What was Cupid's FY26 revenue?

Cupid reported FY26 revenue of ₹358 crore, exceeding management guidance.

- What percentage return has Cupid delivered in five years?

The stock has generated approximately 8,215% returns over the past five years based on the chart shared.

- What is Cupid's FY27 guidance?

Management has guided for revenue of ₹600 crore and net profit of ₹180 crore in FY27.

- Did promoters recently buy shares?

Yes. Chairman and Managing Director Aditya Kumar Halwasiya acquired 21 lakh shares through open market purchases in June 2026.