Shares of G R Infraprojects Limited (NSE:GRINFRA) declined nearly 6% in the latest trading session around ₹937 after the company reported mixed Q4FY26 results. While revenue growth remained healthy and the order book strengthened significantly, investors reacted negatively to margin compression and lower consolidated profitability during the quarter.

The infrastructure company continued to demonstrate strong execution capabilities across roads, railways, tunnels, transmission, and logistics infrastructure projects. However, softer margins and weaker operational profitability weighed on market sentiment.

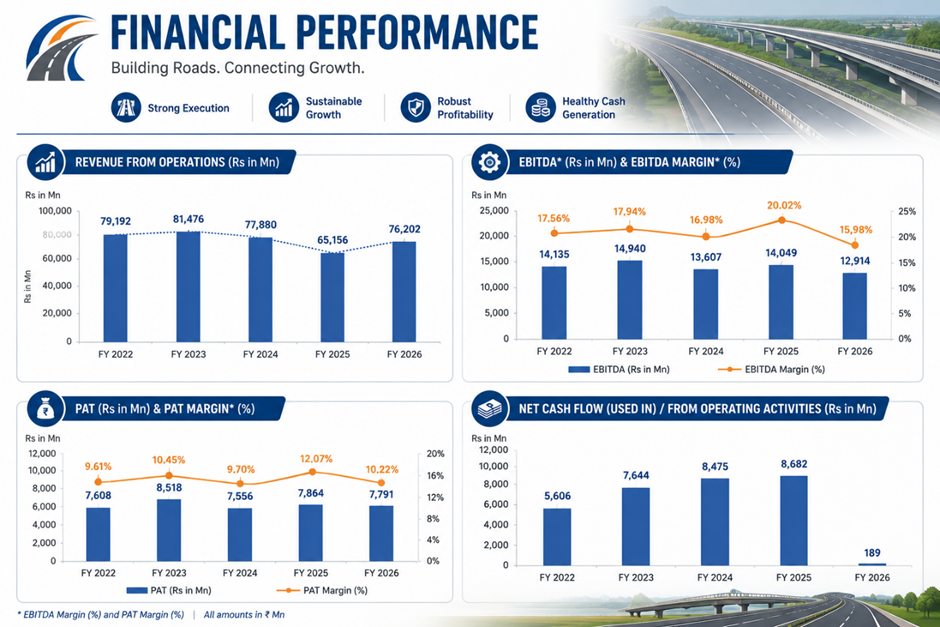

Data Source: Company Filing; Image source: © 2026 Krish Capital Pty. Ltd., Analysis: Kalkine Group

Revenue Growth Supported by Strong Project Execution

G R Infraprojects reported standalone total income of ₹26,197 million in Q4FY26, registering strong growth of 23% year-on-year compared to ₹21,293 million in Q4FY25. Revenue from operations increased 26.65% YoY to ₹25,209 million, reflecting healthy execution momentum across infrastructure projects.

For the full year FY26, standalone revenue from operations rose to ₹76,202 million compared to ₹65,156 million in FY25, indicating sustained project activity and execution strength.

Despite strong top-line growth, standalone EBITDA declined 21.5% YoY to ₹2,734 million in Q4FY26 due to rising construction expenses and margin pressure. EBITDA margin contracted sharply to 10.85% from 17.51% in Q4FY25. The company noted that adjusted EBITDA margins were impacted by changes in labour laws and lower bonus/claim adjustments during the quarter.

PAT Supported by Exceptional Gains

Standalone profit after tax (PAT) increased 12.4% YoY to ₹4,173 million during Q4FY26. However, the profit growth was largely supported by exceptional gains from the transfer of operational HAM projects to Indus Infra Trust.

The company recognized an exceptional gain of nearly ₹1,817 million (net of tax) from the sale of three operational HAM projects during the quarter. Excluding these one-time gains, profitability remained relatively softer due to margin compression and rising operational costs.

On a consolidated basis, PAT declined sharply by nearly 48% YoY to ₹2,099 million in Q4FY26 compared to ₹4,032 million in the corresponding quarter last year. Consolidated EBITDA margin also weakened to 14.73% from 23.96% in Q4FY25.

Robust Order Book Strengthens Long-Term Visibility

One of the biggest positives from the quarter remained G R Infraprojects’ strong order pipeline. The company’s order book stood at ₹264,715 million as of March 31, 2026, providing healthy long-term revenue visibility.

Road projects continue to dominate the portfolio, contributing nearly 69% of the total order book, while transmission, tunnels, railways, telecom infrastructure, and logistics projects contribute to diversification. NHAI remains the largest client, accounting for nearly 62% of total orders.

The company also continued expanding into emerging infrastructure opportunities including Battery Energy Storage Systems (BESS), telecom infrastructure, ropeways, and multi-modal logistics parks. Management highlighted that the company emerged as the lowest bidder for its first BESS project during FY26.

Strong Balance Sheet and Operational Efficiency

G R Infraprojects maintained relatively healthy leverage metrics during FY26. Standalone debt stood at ₹3,153 million while cash and bank balances were higher at ₹6,670 million, supporting a net cash position.

The company’s standalone net debt-to-equity ratio improved significantly over the years and stood near 0.03x during FY26, reflecting disciplined financial management.

Management also emphasized the company’s integrated business model, in-house manufacturing capabilities, and strong project execution framework as key competitive advantages supporting long-term growth.

Technical Summary

GRINFRA shares remain under pressure despite recent recovery attempts. The stock is trading marginally above the 51-day EMA near ₹919, indicating consolidation after prolonged weakness. RSI around 53 reflects neutral momentum conditions. Immediate resistance is visible near ₹980–1,000, while support is positioned near ₹900 amid ongoing volatility.

Chart by TradingView

Conclusion

G R Infraprojects delivered strong revenue growth and maintained a robust order book during FY26, reflecting healthy infrastructure execution capabilities. However, margin compression and weaker consolidated profitability weighed on investor sentiment. Diversification into emerging infrastructure segments, disciplined balance-sheet management, and long-term order visibility continue supporting the company’s broader growth outlook.

FAQs

- Why did GRINFRA shares decline after Q4FY26 results?

Investors reacted negatively to margin contraction and weaker consolidated profitability despite healthy revenue growth and a strong order book.

- What is G R Infraprojects’ current order book?

The company reported a robust order book of ₹264,715 million as of March 31, 2026.

- Which segment contributes most to GRINFRA’s business?

Road infrastructure projects remain dominant, contributing nearly 69% of the company’s total order book during FY26.