Shares of The New India Assurance Company Limited (NSE:NIACL) remained under pressure in the latest trading session, declining nearly 2.7% to around ₹158.8 despite the state-owned general insurer reporting strong profit growth for Q4FY26 and FY26. Investor sentiment remained cautious amid elevated claims ratios, competitive pressure in motor insurance, and higher operating costs linked to wage revisions.

The company, however, delivered healthy premium growth, improved profitability, and higher market share during FY26, reinforcing its leadership position in India’s general insurance sector.

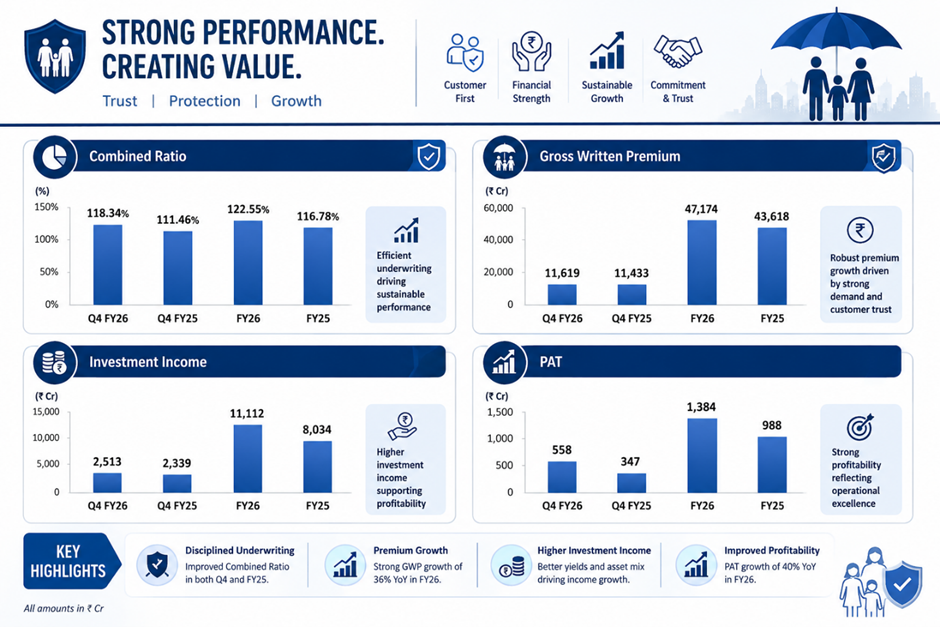

Data Source: Company Filing; Image source: © 2026 Krish Capital Pty. Ltd., Analysis: Kalkine Group

PAT Rises 40% in FY26 on Better Investment Income

The New India Assurance reported profit after tax (PAT) of ₹1,384 crore in FY26, registering a robust 40% year-on-year increase compared to ₹988 crore in FY25. Q4FY26 PAT also surged 61% YoY to ₹558 crore from ₹347 crore in the corresponding quarter last year.

Gross Written Premium (GWP) rose 8.15% YoY to ₹47,174 crore during FY26, while Q4FY26 GWP increased 1.63% to ₹11,619 crore. The company’s Indian business outpaced industry growth, with domestic premium growth of 10.9% compared to overall industry growth of 9.3%. Market share improved from 12.56% to 12.74% during FY26.

Investment income remained a major earnings driver, rising sharply to ₹11,112 crore in FY26 from ₹8,034 crore in FY25. Higher capital gains and stronger investment returns partially offset underwriting pressure during the year.

Claims Pressure and Wage Revision Impact Underwriting Performance

Despite healthy profit growth, underwriting profitability remained under pressure. The combined ratio rose to 122.57% in FY26 compared to 116.78% in FY25, while the incurred claims ratio increased to 98.65% from 96.61%.

Management attributed the deterioration primarily to elevated loss ratios in the Motor Third Party segment, where premium revisions are still pending. Aviation losses and competitive pricing pressure in the motor business also weighed on margins during the year.

Additionally, the insurer absorbed the full impact of wage revision and family pension revisions amounting to ₹3,525 crore during FY26. Of this, approximately ₹597 crore related to pension revision impact was recognized in Q4FY26 alone.

Underwriting results were negatively impacted by employee-related provisions of ₹2,314 crore during FY26, while retired employee benefit expenses added further pressure to operating profitability.

Health Segment Growth and Strong Solvency Support Outlook

The Health & Personal Accident segment continued to remain the company’s largest business vertical, contributing nearly 47.6% of total gross written premium. The segment delivered FY26 premium growth of 12.62% YoY to ₹22,444 crore.

The company maintained a healthy solvency ratio of 1.84x, comfortably above regulatory requirements, while assets under management stood at ₹96,652 crore at the end of FY26. Net worth also improved to ₹23,619 crore.

Management stated that the company remains optimistic about FY27 growth prospects with a stronger focus on retail, MSME, and non-motor insurance segments. The insurer is also expanding into newer categories such as parametric insurance and strengthening digital capabilities through AI-enabled customer service and multilingual support platforms.

Technical Summary

NIACL shares are trading slightly above the 51-day EMA near ₹152.7, indicating stabilizing momentum after recent recovery from lower levels. RSI near 53 reflects neutral momentum conditions. The stock faces resistance around ₹165–170, while support is visible near ₹150. Sustained breakout above current consolidation could improve medium-term sentiment.

Chart by TradingView

Conclusion

The New India Assurance delivered strong FY26 profit growth supported by robust investment income and healthy premium expansion despite elevated claims pressure and wage revision impacts. While underwriting profitability remains challenging, improving market share, strong solvency, and retail-focused growth initiatives position the insurer for stable long-term expansion in India’s growing insurance market.

FAQs

- Why did NIACL shares fall despite higher profits?

Investors remained cautious due to elevated claims ratios, underwriting losses, and higher employee-related expenses despite strong PAT growth.

- What was New India Assurance’s FY26 profit?

The company reported FY26 PAT of ₹1,384 crore, up 40% year-on-year from ₹988 crore in FY25.

- Which segment contributed most to NIACL premiums?

Health & Personal Accident remained the largest segment, contributing nearly 47.6% of total gross written premium during FY26.