India’s high-precision engineering space is witnessing rising investor attention, and MTAR Technologies Limited (NSE:MTARTECH) is emerging as one of the key beneficiaries of this structural shift. The company is steadily expanding its presence across nuclear energy, aerospace, defence, fuel cells, hydel systems, and next-generation clean energy technologies sectors increasingly linked with the global AI and advanced infrastructure boom.

With strong order inflows, rising international exposure, and growing participation in critical engineering programs, MTAR Technologies appears to be positioning itself for long-term high-value opportunities.

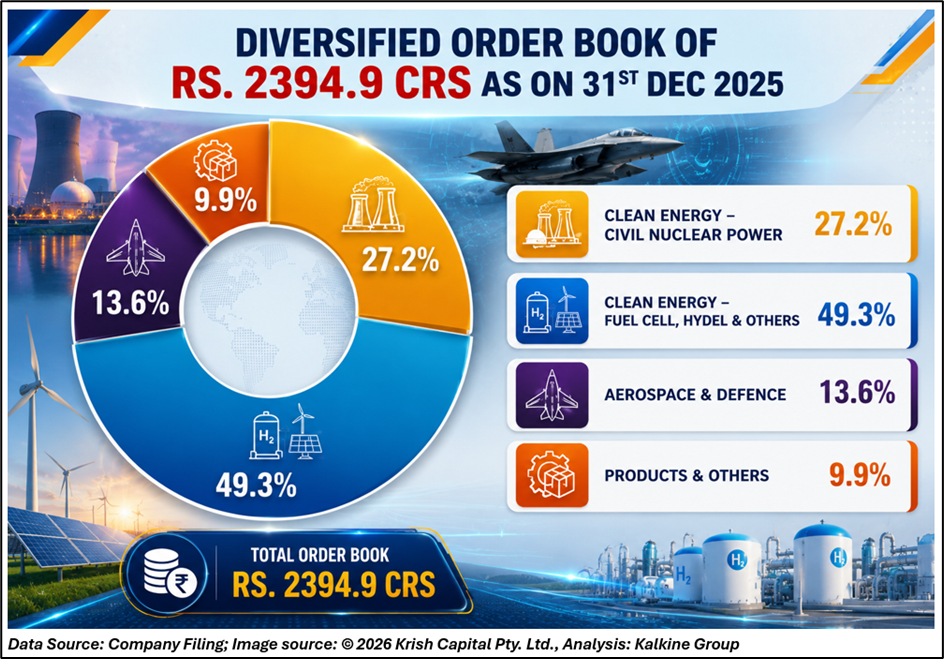

Strong Order Book Signals Growth Visibility

MTAR Technologies reported a diversified order book of ₹2,394.9 crore as of December 31, 2025, supported by major order inflows across clean energy, aerospace & defence, and nuclear power segments.

The company also announced fresh purchase orders worth ₹2,278.96 crore from an international customer, highlighting continued demand momentum in its advanced engineering business.

Management indicated that these orders are part of ongoing business relationships with existing global customers, reflecting sustained confidence in MTAR’s manufacturing capabilities.

Why AI Infrastructure Could Benefit MTAR

The global artificial intelligence boom is driving massive investments into energy-intensive infrastructure including data centres, power systems, advanced cooling technologies, and clean energy solutions.

As AI adoption accelerates globally, demand for reliable nuclear energy, hydrogen systems, battery storage, and precision-engineered industrial equipment is expected to rise significantly.

MTAR’s presence in critical clean-energy components, fuel cell systems, hydel infrastructure, and nuclear engineering may position it to indirectly benefit from this long-term infrastructure cycle.

The company already serves sectors where precision engineering, reliability, and complex manufacturing capabilities are key competitive advantages.

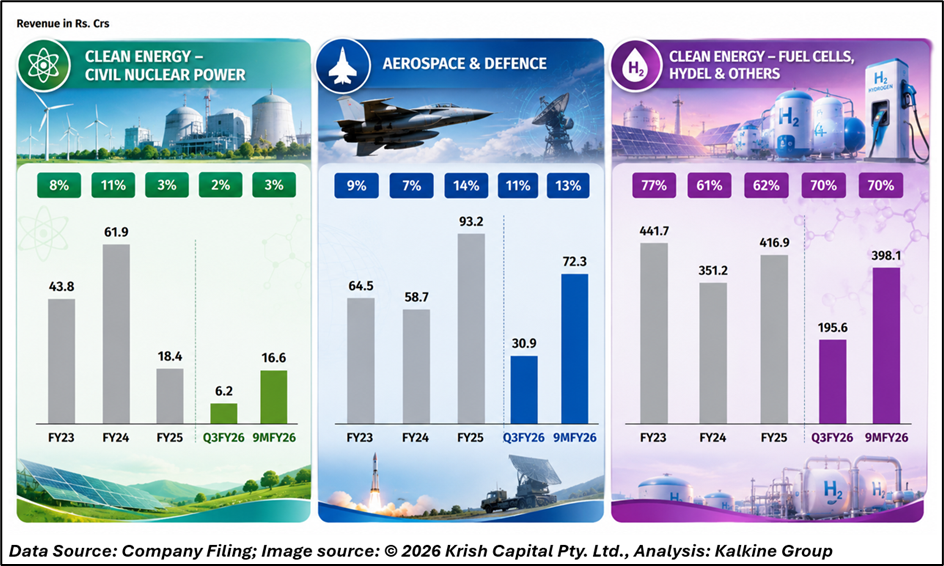

Nuclear and Clean Energy Remain Major Growth Drivers

According to the company’s investor presentation, nearly 70% of MTAR’s 9MFY26 revenue came from the Clean Energy – Civil Nuclear Power segment.

The company has also been strengthening its capabilities in:

- Civil nuclear power systems

- Fuel cells and hydrogen technologies

- Hydel and renewable energy systems

- Aerospace and defence engineering

- Battery storage-related infrastructure

Its expanding customer base includes global names across aerospace, clean energy, and industrial engineering sectors.

Aerospace and Defence Expansion Adds Diversification

Beyond clean energy, MTAR is also seeing traction in aerospace and defence manufacturing.

The company highlighted ongoing production programs for global aerospace players including:

- GKN Aerospace

- Thales

- Rafael

- Collins Aerospace

- Israel Aerospace Industries (IAI)

Management stated that batch production for several new aerospace products has commenced and could become a major revenue contributor from FY26 onward.

Financial Performance Shows Strong Momentum

MTAR Technologies delivered robust Q3 FY26 performance, reflecting strong execution and operating leverage.

Key highlights include:

- Revenue from operations rose 59.3% YoY to ₹278 crore

- EBITDA increased 92.5% YoY to ₹64 crore

- PAT surged 117.3% YoY to ₹34.7 crore

- EBITDA margin improved to 23% in Q3 FY26

The company’s gross profit for Q3 FY26 stood at ₹128.1 crore, while 9MFY26 revenue reached ₹570.1 crore.

Key Risks Investors Should Monitor

Despite strong growth visibility, investors should continue monitoring:

- Working capital intensity

- Execution timelines for large projects

- Dependence on government-linked sectors

- Cyclicality in defence and energy capex

- Margin fluctuations due to raw material costs

The company’s working capital cycle remains elevated due to the nature of large engineering and project-based contracts.

Technical Summary

MTAR Technologies is currently trading with strong bullish momentum, hovering near ₹7,181 after a sharp rally above its 51-day EMA around ₹4,880. RSI near 76 indicates strong buying strength but also signals stretched near-term conditions. Trend remains firmly positive, although intraday volatility or temporary profit-booking may emerge at higher levels.

Chart by TradingView

Outlook

MTAR Technologies is increasingly positioning itself at the intersection of several long-term structural themes including nuclear energy, aerospace manufacturing, hydrogen systems, and AI-linked infrastructure expansion.

With a strong order pipeline, improving profitability, and growing participation in high-value engineering programs, the company may continue attracting investor interest as India’s advanced manufacturing ecosystem expands globally.

FAQs

- Why is MTAR Technologies gaining investor attention?

MTAR is benefiting from rising opportunities in nuclear power, aerospace, defence, hydrogen systems, and clean energy infrastructure.

- How is AI linked to MTAR Technologies?

The AI boom is increasing demand for energy infrastructure, advanced engineering systems, and clean power solutions where MTAR operates.

- What is MTAR Technologies’ latest order book size?

The company reported an order book of approximately ₹2,394.9 crore as of December 2025.