Highlights

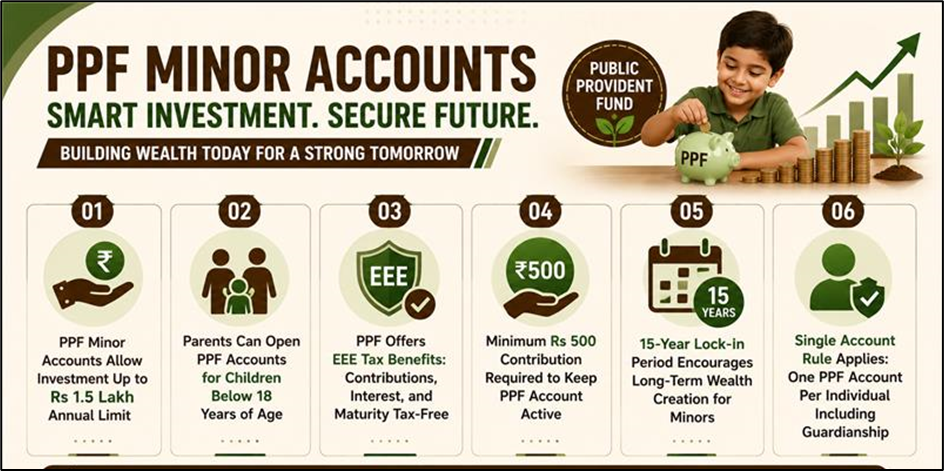

- Parents or legal guardians can open PPF accounts for minor children.

• Annual combined investment limit remains capped at Rs 1.5 lakh.

• PPF continues to provide tax-free returns under EEE structure rules.

The Public Provident Fund (PPF) is a government-supported long-term savings scheme that allows parents or legal guardians to open and manage accounts for children below 18 years of age. The objective of this facility is to encourage disciplined long-term savings from an early stage of life.

The account remains under guardian control until the child reaches adulthood. After turning 18, ownership and operational control are transferred to the account holder, enabling independent management of funds.

Source: Analysis by Kalkine

Eligibility and Account Opening Structure

A PPF account for a minor can only be opened through a parent or legal guardian. The scheme allows only one guardian to operate the account at any given time, ensuring clear accountability.

Each individual is permitted to maintain only one PPF account in their name. Even if multiple accounts exist for different children, the system ensures that compliance rules regarding ownership and operation are strictly followed.

Investment Limit and Contribution Rules

The PPF scheme sets a maximum annual investment limit of Rs 1.5 lakh per financial year. This ceiling applies collectively to all accounts linked to one individual, including their personal account and any accounts maintained as a guardian for minors.

To keep the account active, a minimum yearly contribution of Rs 500 is required. If this condition is not met, the account may become inactive and will require formal procedures to reactivate it.

These limits are designed to maintain uniformity and prevent excess use of tax-advantaged investment channels.

Tax Treatment Under PPF Scheme

PPF follows the Exempt-Exempt-Exempt (EEE) taxation structure. This means contributions made, interest earned during the tenure, and maturity proceeds are generally exempt from tax under applicable conditions.

However, eligibility for deduction under Section 80C is available only under the old tax regime. Individuals opting for the new tax regime cannot claim such deductions, although the scheme’s interest and maturity benefits remain governed by its tax-free structure.

Long-Term Savings Purpose

PPF accounts for minors are commonly used as a structured method for building long-term savings. Parents often invest with long-term goals such as higher education, marriage, or other future financial needs in mind.

The 15-year lock-in period encourages disciplined investing, while compounding helps build a larger corpus over time. Once the child becomes an adult, the account can either continue or be extended as per scheme provisions.

Operational and Compliance Conditions

The scheme does not allow multiple PPF accounts for a single individual. If such situations occur, regulatory correction procedures may apply.

Proper documentation is required at the time of opening a minor account, including valid proof of guardianship. In general, only parents or legally appointed guardians can operate the account until the child attains majority.

Key Risks

- Contribution limit may restrict other tax-saving investment options.

- Non-payment of minimum amount can lead to account deactivation.

- Incorrect guardian details may create compliance issues later.

- Tax benefits depend on the income tax regime selected.

Summary

PPF accounts for minors provide a structured savings option under guardian supervision, combining long-term discipline with government-backed returns. While the scheme offers tax efficiency and capital safety, strict rules on contribution limits, eligibility, and documentation must be followed. The overall effectiveness of the account depends on consistent investment behaviour and proper compliance with scheme guidelines.

FAQs

Q: Can a parent open a PPF account for a child?

A: Yes, parents or legal guardians can open and operate a PPF account until the child reaches adulthood.

Q: Is the investment limit shared between parent and child accounts?

A: Yes, the total combined contribution limit across accounts is Rs 1.5 lakh per financial year.

Q: Are returns from minor PPF accounts taxable?

A: No, PPF returns remain tax-free under the scheme’s exempt taxation structure rules.