Understanding How Capital Gains Tax Works on Equity Investments and Mutual Funds in India

Investing in stocks and mutual funds has become increasingly popular among Indian investors seeking long-term wealth creation, financial security, and participation in economic growth. While investment returns can significantly enhance personal wealth, it is equally important to understand the tax implications associated with these gains.

One of the most important aspects of investment taxation in India is Capital Gains Tax. Whenever an investor earns a profit by selling stocks or mutual fund units, the gain may be subject to taxation depending on factors such as the type of asset, holding period, and applicable tax regulations.

A clear understanding of capital gains taxation can help investors make informed decisions, improve tax planning, and optimize post-tax investment returns.

This article explains how capital gains tax on stocks and mutual funds works in India, including the distinction between Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG), applicable tax rates, and key considerations for investors.

What Is Capital Gains Tax?

Capital Gains Tax is the tax levied on the profit earned from the sale of a capital asset. In the context of investments, capital assets may include:

- Listed equity shares

- Equity mutual funds

- Debt mutual funds

- Exchange Traded Funds (ETFs)

- Bonds and other securities

The taxable gain is generally calculated as:

Capital Gain = Sale Value – Purchase Cost – Eligible Expenses

The tax liability depends primarily on how long the investment was held before being sold.

Understanding Short-Term and Long-Term Capital Gains

Capital gains are classified into two categories:

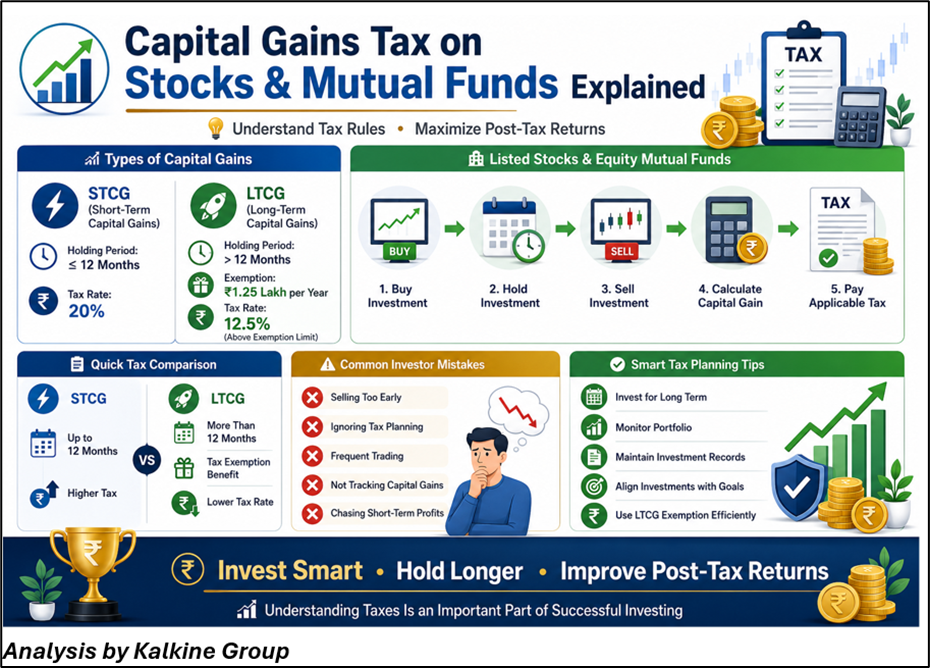

Short-Term Capital Gains (STCG)- A gain is considered short-term when the investment is sold within the specified holding period.

For:

- Listed equity shares

- Equity-oriented mutual funds

- Equity ETFs

investments held for 12 months or less are generally classified as short-term assets.

Long-Term Capital Gains (LTCG)- Investments held beyond the prescribed holding period qualify as long-term capital assets.

For listed equities and equity-oriented mutual funds, investments held for more than 12 months are generally treated as long-term holdings.

Capital Gains Tax on Listed Equity Shares & Short-Term Capital Gains Tax on Stocks

When listed shares are sold within 12 months of purchase and Securities Transaction Tax (STT) has been paid, the gains are generally taxed at:

STCG Tax Rate: 20% under applicable provisions of the Income Tax framework.

This tax is applied irrespective of the investor's income tax slab.

Long-Term Capital Gains Tax on Stocks- If listed equity shares are held for more than 12 months, gains qualify as long-term capital gains.

Key provisions include:

- Annual LTCG exemption up to ₹1.25 lakh

- Gains exceeding the exemption limit are generally taxed at 12.5%

- Indexation benefit is generally not available for listed equity investments under this category

For long-term investors, the exemption threshold provides a degree of tax efficiency while encouraging wealth creation through equity participation.

Capital Gains Tax on Equity Mutual Funds- Equity-oriented mutual funds generally receive tax treatment similar to listed equity shares because a substantial portion of their portfolio is invested in equities.

Short-Term Capital Gains on Equity Mutual Funds- If units are redeemed within 12 months.

- Gains are generally taxed at 20%.

Long-Term Capital Gains on Equity Mutual Funds- If units are held for more than 12 months.

- LTCG up to ₹1.25 lakh in a financial year is generally exempt.

- Gains above this threshold are taxed at 12.5%.

These provisions make equity mutual funds a popular long-term investment vehicle among retail investors.

Taxation of Debt Mutual Funds- Debt mutual funds follow a different taxation framework.

For many debt-oriented mutual fund investments acquired after specified regulatory changes, capital gains are generally taxed according to the investor's applicable income tax slab rather than receiving preferential long-term capital gains treatment.

Investors should evaluate tax implications carefully when comparing debt funds with other fixed-income investment alternatives.

Understanding Securities Transaction Tax (STT)- Securities Transaction Tax (STT) is a tax levied on the purchase and sale of certain securities traded on recognized stock exchanges.

STT plays an important role because concessional capital gains tax rates on listed equities and equity mutual funds are generally linked to compliance with STT requirements.

Investors should ensure that transactions meet the applicable conditions to qualify for favorable tax treatment.

How Capital Gains Are Calculated

The basic calculation involves determining the difference between the selling price and acquisition cost.

Example

Suppose an investor:

- Purchases shares worth ₹2,00,000

- Sells them after two years for ₹3,50,000

Capital Gain:

₹3,50,000 – ₹2,00,000 = ₹1,50,000

If the investment qualifies as LTCG:

- Exemption: ₹1,25,000

- Taxable Gain: ₹25,000

- Applicable LTCG tax may be calculated on the taxable portion as per prevailing regulations.

Actual tax liability may vary depending on individual circumstances and prevailing tax provisions.

Tax Planning Strategies for Investors

While tax should not be the sole basis for investment decisions, efficient tax planning can improve net investment returns.

Some commonly used approaches include:

- Holding Investments for the Long Term- Longer holding periods may qualify investments for more favorable LTCG treatment.

- Utilizing Annual LTCG Exemption Limits- Investors may consider planned profit-booking strategies within permissible exemption thresholds.

- Maintaining Proper Investment Records- Accurate documentation of purchase dates, acquisition costs, and transaction details helps simplify tax calculations and compliance.

- Aligning Investments with Financial Goals- Tax planning works most effectively when integrated with broader financial planning objectives rather than being treated as an isolated exercise.

Common Mistakes Investors Should Avoid-

Many investors unintentionally increase their tax burden due to poor planning.

Common mistakes include:

- Ignoring holding periods before selling investments

- Failing to track capital gains accurately

- Frequently churning portfolios

- Overlooking tax implications during profit booking

- Making investment decisions solely for tax-saving purposes

A balanced approach focused on both returns and tax efficiency can improve long-term investment outcomes.

Conclusion

Capital Gains Tax is an important component of investment planning for Indian investors. Understanding the distinction between short-term and long-term capital gains, applicable tax rates, exemption limits, and holding period requirements can help investors make more informed financial decisions.

While taxation may reduce a portion of investment returns, disciplined investing, long-term wealth creation strategies, and effective tax planning can significantly enhance post-tax outcomes.

For investors participating in stocks and mutual funds, a strong understanding of capital gains taxation is essential for maximizing financial efficiency and achieving long-term investment goals.

Frequently Asked Questions (FAQs)

- What is the difference between STCG and LTCG on stocks?

Short-Term Capital Gains arise when listed shares are sold within 12 months of purchase, while Long-Term Capital Gains apply when shares are held for more than 12 months before being sold.

- Is LTCG on equity mutual funds taxable in India?

Yes. Long-term capital gains exceeding the applicable annual exemption threshold of ₹1.25 lakh are generally taxed at 12.5% under prevailing regulations.

- Are debt mutual funds taxed differently from equity mutual funds?

Yes. Debt mutual funds generally follow different tax rules, and taxation may depend on acquisition date, holding period, and prevailing regulations. In many cases, gains are taxed according to the investor's income tax slab.