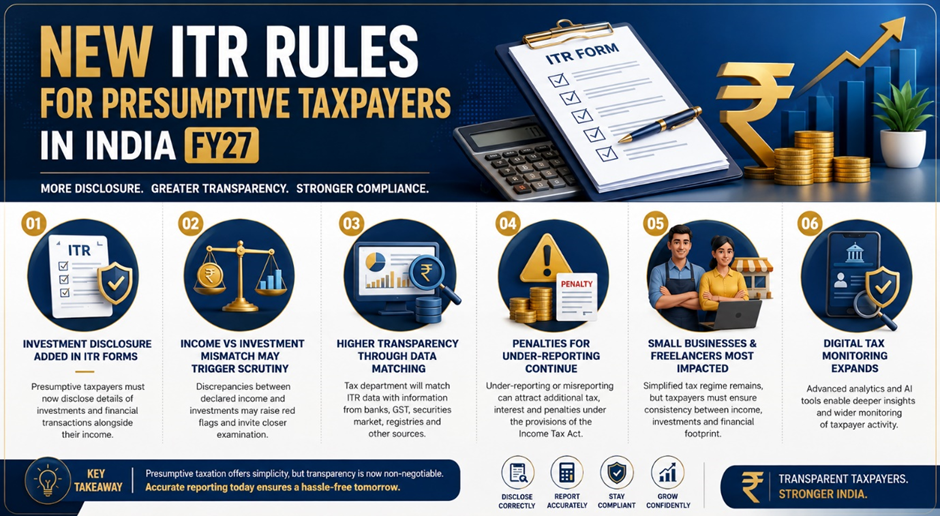

India’s income tax filing framework is witnessing another significant compliance-focused shift. In the latest Income Tax Return (ITR) forms, taxpayers opting for the presumptive taxation scheme are now required to disclose details of investments and major financial activities alongside their declared income. The move is aimed at strengthening transparency and improving data matching capabilities for the Income Tax Department.

The development could have far-reaching implications for small businesses, professionals, freelancers, and self-employed individuals who commonly rely on presumptive taxation to simplify tax filing procedures.

Analysis Kalkine Group

Investment Disclosure Now Linked with Presumptive Income Reporting

Under the presumptive taxation regime, eligible taxpayers can declare income at a prescribed percentage of turnover without maintaining detailed books of accounts. While the system was designed to reduce compliance burden for smaller taxpayers, authorities are increasingly focusing on ensuring that declared income aligns with actual financial behaviour.

The revised ITR forms now include additional disclosure requirements related to investments, expenditure patterns, and financial transactions. This means taxpayers choosing presumptive taxation may have to report assets, investments, or other high-value transactions even if they are not maintaining extensive accounting records.

Experts believe the government is attempting to bridge the gap between simplified taxation and financial transparency by enabling better cross-verification of income declarations against lifestyle indicators and investment activities.

Mismatch Between Income and Investments May Invite Scrutiny

Tax professionals caution that inconsistencies between reported presumptive income and disclosed investments could attract closer examination from tax authorities.

For instance, if a taxpayer declares relatively modest income under the presumptive scheme but simultaneously reports sizeable investments in mutual funds, property, equities, insurance products, or luxury assets, the discrepancy may raise questions regarding the actual source of funds.

The enhanced disclosure framework is expected to strengthen data analytics-based scrutiny, where authorities can compare ITR information with data available from banks, registrars, financial institutions, securities markets, and GST filings.

With digitisation of tax monitoring systems accelerating, authorities now possess stronger capabilities to identify abnormal financial patterns and potential under-reporting of income.

Penalties for Incorrect Reporting Continue

The updated forms do not alter existing penalty provisions related to inaccurate reporting. Taxpayers may continue to face consequences for under-reporting or misreporting income if discrepancies are detected during assessment.

Depending on the nature and severity of the mismatch, penalties could include additional tax liability, interest payments, and financial penalties under applicable provisions of the Income Tax Act.

In certain cases, authorities may also question whether the taxpayer genuinely qualifies for the presumptive taxation scheme if the disclosed financial profile appears inconsistent with the income reported.

Greater Compliance Expectations for Small Taxpayers

The changes indicate that simplified tax regimes no longer guarantee reduced scrutiny. Even taxpayers benefiting from easier filing mechanisms may now need to maintain stronger financial documentation and ensure consistency across investments, banking transactions, and tax declarations.

Industry observers believe the revised ITR framework reflects the government’s broader strategy of widening the tax base while leveraging technology-driven compliance monitoring.

For small businesses and professionals, the focus may now shift toward maintaining better financial discipline, accurate disclosures, and stronger alignment between reported income and actual spending or investment capacity.

Conclusion

The addition of investment disclosure columns in ITR forms marks a notable compliance upgrade for presumptive taxpayers. While the presumptive scheme continues to offer simplified tax filing benefits, the latest changes signal tighter scrutiny around financial transparency and income consistency. Taxpayers may need to exercise greater caution while reporting income and investments to avoid potential notices, penalties, or compliance challenges in the future.

FAQs

- What is the new change for presumptive taxpayers in ITR forms?

The updated ITR forms now require presumptive taxpayers to disclose certain investments and financial transactions alongside income reporting.

- Why has the government added investment disclosure columns?

The move aims to improve transparency and help authorities match declared income with investments and spending patterns.

- Can mismatched income and investments trigger tax scrutiny?

Yes, large investments compared to reported presumptive income may attract closer examination from tax authorities.

- Are penalties applicable for incorrect reporting under presumptive taxation?

Penalties for under-reporting or misreporting income continue to apply under existing Income Tax provisions.

- Who will be most affected by the revised ITR disclosure rules?

Small businesses, freelancers, professionals, and self-eployed individuals using presumptive taxation could face higher compliance expectations.