A Comprehensive Guide to Reducing Tax Liability and Enhancing Financial Security During Retirement

Retirement marks the beginning of a new phase of life—one that offers greater freedom, flexibility, and the opportunity to enjoy the rewards of years of hard work. However, retirement also brings unique financial challenges. Managing fixed income sources, rising healthcare costs, inflation, and evolving tax regulations requires careful planning to ensure long-term financial stability.

For senior citizens in India, effective tax planning is not merely about reducing tax liability; it is about preserving retirement income, improving cash flow, and safeguarding financial independence. Fortunately, the Indian tax framework provides several benefits and provisions specifically designed to support senior and super senior citizens.

By understanding available deductions, exemptions, investment options, and tax-efficient income strategies, retirees can optimize their finances and make the most of their retirement years.

Why Tax Planning Matters for Senior Citizens

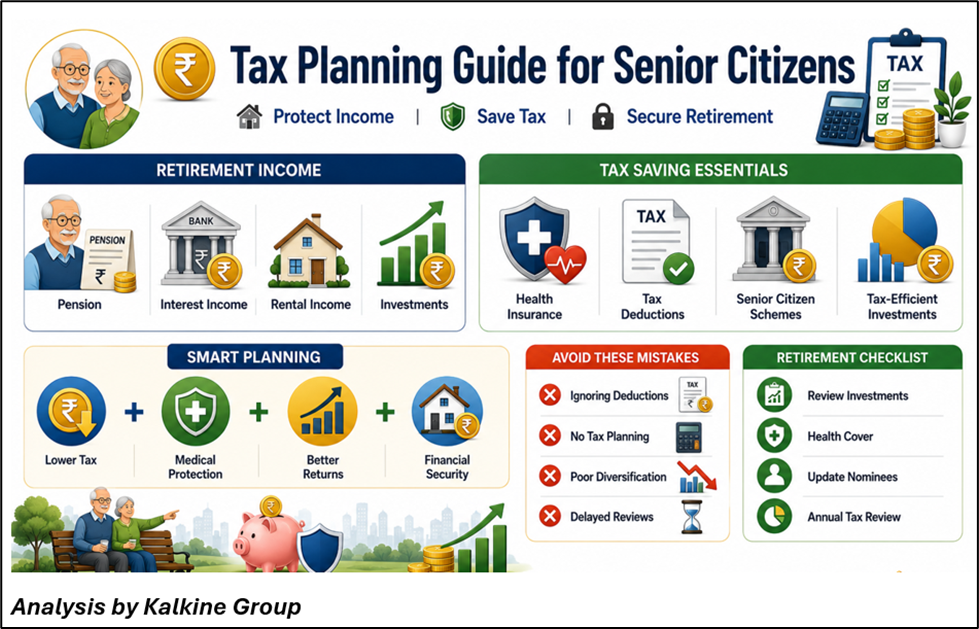

Many retirees assume that tax planning becomes less important after retirement due to the absence of regular employment income. However, pension income, interest earnings, rental income, capital gains, and other investment returns may still attract taxation.

A structured tax plan can help senior citizens:

- Reduce overall tax liability

- Preserve retirement savings

- Improve post-tax income

- Manage healthcare expenses efficiently

- Enhance financial security

- Ensure effective wealth transfer planning

Thoughtful tax management becomes increasingly important when income generation opportunities are limited during retirement.

Understanding Tax Benefits Available to Senior Citizens

The Income Tax Act provides certain benefits specifically for senior citizens.

For tax purposes:

- Senior Citizens are individuals aged 60 years or above but below 80 years.

- Super Senior Citizens are individuals aged 80 years or above.

These categories often receive favorable tax treatment through higher exemption limits and additional deductions under various provisions.

Understanding these benefits is the foundation of effective retirement tax planning.

Optimize Tax-Efficient Investment Income

Retirement income often comes from investments rather than salaries. Therefore, selecting tax-efficient investment avenues is critical.

Senior citizens commonly derive income from:

- Fixed deposits

- Senior Citizen Savings Schemes

- Monthly income plans

- Bonds

- Mutual funds

- Rental properties

- Dividend-paying investments

A diversified investment strategy that balances income generation, capital preservation, and tax efficiency can significantly improve overall financial outcomes.

Investors should periodically review their portfolios to ensure that investments remain aligned with retirement objectives and evolving tax regulations.

Utilize Section 80C Deductions Effectively

Certain eligible investments and expenditures may qualify for tax deductions under Section 80C.

Common options may include:

- Tax-saving fixed deposits

- Life insurance premiums

- Public Provident Fund contributions

- Eligible investment instruments prescribed under tax regulations

Proper utilization of available deductions can help reduce taxable income while supporting broader financial goals.

Senior citizens should evaluate these options based on liquidity needs, risk tolerance, and investment objectives.

Benefit from Health Insurance Tax Deductions

Healthcare expenses often become a significant component of retirement planning. As medical costs continue to rise, maintaining adequate health insurance coverage becomes increasingly important.

Premiums paid toward eligible health insurance policies may qualify for deductions under applicable provisions of the Income Tax Act.

These deductions can help:

- Lower taxable income

- Reduce healthcare-related financial risks

- Protect retirement savings from unexpected medical expenses

Health insurance should be viewed not only as a tax-saving tool but also as a critical component of retirement financial security.

Plan Interest Income Efficiently

Interest income from fixed deposits, savings accounts, and other interest-bearing investments forms a substantial portion of retirement earnings for many senior citizens.

While interest income may be taxable, retirees should remain aware of applicable exemptions, deductions, and reporting requirements.

Regular review of investment allocation can help optimize after-tax returns while maintaining adequate liquidity and capital preservation.

Balancing fixed-income investments with other tax-efficient instruments may improve overall portfolio performance.

Consider Tax-Efficient Mutual Fund Investments

Mutual funds can provide diversification, professional management, and potential tax advantages depending on the investment category and holding period.

For senior citizens seeking long-term wealth preservation and inflation protection, mutual funds may serve as an effective complement to traditional fixed-income investments.

Before investing, retirees should carefully evaluate:

- Risk profile

- Investment horizon

- Liquidity requirements

- Income needs

- Tax implications

A balanced approach can help achieve both growth and stability during retirement.

Manage Capital Gains Strategically

Many senior citizens hold long-term investments accumulated over several decades. The sale of such assets may result in capital gains taxation.

Proper planning can help retirees:

- Manage tax liabilities effectively

- Utilize available exemptions where applicable

- Schedule asset sales strategically

- Preserve investment returns

Capital gains planning should be integrated into broader retirement and estate planning strategies.

Maintain Proper Documentation

Tax compliance becomes significantly easier when financial records are organized and readily accessible.

Important documents may include:

- Pension statements

- Interest certificates

- Investment records

- Insurance premium receipts

- Capital gains statements

- Tax deduction certificates

Accurate documentation helps simplify return filing and reduces the likelihood of errors or compliance issues.

Review Tax Planning Annually

Tax regulations, personal circumstances, healthcare needs, and investment portfolios can change over time.

An annual review helps ensure that:

- Tax-saving opportunities are utilized effectively

- Investments remain aligned with retirement goals

- Income strategies remain tax-efficient

- Financial plans adapt to changing circumstances

Regular assessment can contribute significantly to long-term financial security.

Estate and Wealth Transfer Planning

Effective retirement planning extends beyond managing current income and taxes. Senior citizens should also consider estate planning and wealth transfer strategies.

Proper planning can help:

- Facilitate smooth asset transfer

- Reduce legal complications

- Protect family interests

- Ensure financial wishes are fulfilled

Preparing wills, reviewing nominations, and organizing financial documentation are important steps in comprehensive financial planning.

Common Tax Planning Mistakes Senior Citizens Should Avoid

Several common mistakes can reduce tax efficiency and affect retirement finances.

These include:

- Ignoring available deductions and exemptions

- Concentrating all savings in low-yield investments

- Delaying tax planning until year-end

- Failing to review investment portfolios

- Overlooking healthcare-related tax benefits

- Neglecting estate planning considerations

Avoiding these mistakes can help retirees maximize retirement income and preserve wealth.

Conclusion

Tax planning remains an essential component of financial management even after retirement. For senior citizens, effective tax planning can help preserve retirement income, reduce tax liabilities, manage healthcare expenses, and support long-term financial independence.

By utilizing available deductions, maintaining a diversified investment portfolio, managing capital gains efficiently, and reviewing financial plans regularly, retirees can strengthen their financial position and enjoy greater peace of mind during retirement.

Ultimately, successful retirement planning is not solely about accumulating wealth—it is about preserving, protecting, and using that wealth efficiently to support a comfortable and financially secure lifestyle.

Frequently Asked Questions (FAQs)

1. Why is tax planning important for senior citizens?

Tax planning helps senior citizens reduce tax liability, improve post-tax income, preserve retirement savings, and manage healthcare and living expenses more effectively.

2. Can health insurance help senior citizens save tax?

Yes. Eligible health insurance premiums may qualify for tax deductions under applicable provisions of the Income Tax Act, subject to prevailing limits and conditions.

3. What are the key sources of taxable income for retirees?

Common sources include pension income, interest earnings, rental income, capital gains, dividends, and returns from various investments and financial assets.