Highlights

- Income mismatches with tax records can invite scrutiny during return processing.

- Incorrect deduction claims may result in notices and delayed refunds.

- Careful verification of disclosures can help avoid filing-related complications.

As taxpayers prepare to file their Income Tax Returns (ITRs) for FY26, accuracy has become more important than ever. The Income Tax Department now relies heavily on digital data collected from employers, banks, financial institutions and other reporting agencies to verify information disclosed in tax returns. As a result, even small errors or omissions can lead to notices, additional verification requests or delays in receiving refunds. A careful review of financial records before filing can help taxpayers avoid unnecessary complications.

Source: Analysis by Kalkine

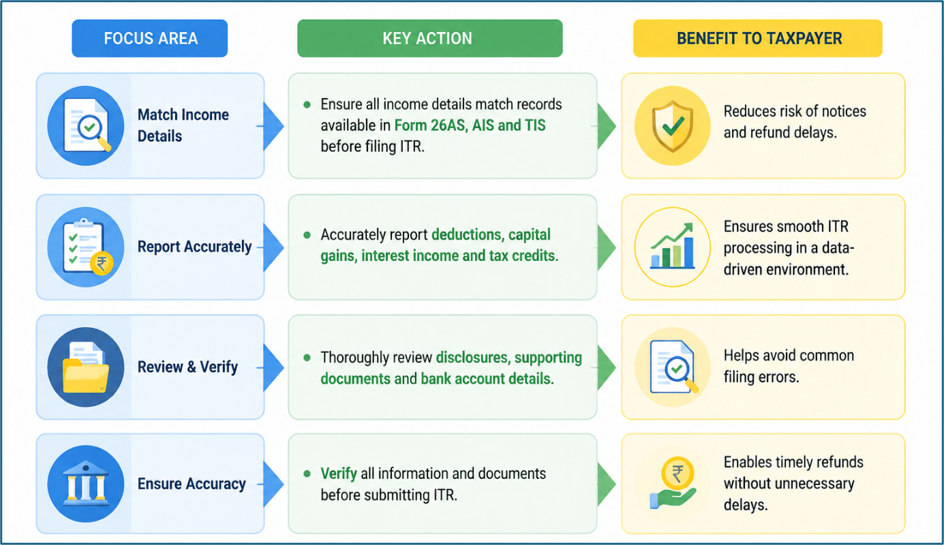

Income Reporting Should Match Official Records

One of the most frequent reasons for tax scrutiny is a mismatch between income reported in an ITR and the information available with the tax department. Salary income, interest earnings, rental income, capital gains and other sources of income should be reported accurately. Taxpayers should compare their return details with information available in Form 26AS, the Annual Information Statement (AIS) and the Taxpayer Information Summary (TIS). Any discrepancy between these records and the filed return may prompt the department to seek clarification.

Deduction Claims Need Proper Support

Taxpayers often claim deductions to reduce their taxable income, but these claims should be supported by valid documentation. Deductions related to tax-saving investments, insurance premiums, home loan repayments and other eligible expenses should reflect actual transactions. Incorrect, inflated or unsupported claims may trigger verification by tax authorities. Maintaining proper records is essential, as taxpayers may be required to provide evidence if their return is selected for review.

Capital Gains Require Accurate Disclosure

Transactions involving shares, mutual funds, real estate and other capital assets deserve particular attention while filing returns. Incorrect calculations, misclassification of gains or losses, or failure to report transactions can lead to scrutiny. Tax authorities receive information about many investment transactions through reporting systems, making it important for taxpayers to reconcile their records and ensure that capital gains are disclosed correctly.

Interest Income Is Commonly Missed

Many taxpayers focus primarily on salary income and overlook interest earned from savings accounts, fixed deposits, recurring deposits and other financial instruments. Since financial institutions report such earnings to tax authorities, failing to include them in an ITR can create discrepancies. Reviewing bank statements and interest certificates before filing can help ensure that all taxable income is accounted for.

Foreign Assets and Overseas Income Need Disclosure

Individuals with foreign bank accounts, overseas investments or income earned outside India may have additional reporting obligations. Incomplete disclosure of foreign assets or income can attract closer scrutiny and potential penalties. Taxpayers with international financial interests should review applicable reporting requirements carefully and ensure that all relevant information is included in their returns.

High-Value Transactions Can Be Examined

Large financial transactions are often reported to tax authorities through various compliance mechanisms. Significant cash deposits, major investments, property purchases and substantial credit card expenditures may be compared against the income disclosed in a tax return. If transaction values appear inconsistent with declared earnings, the taxpayer may be asked to explain the source of funds.

Verify Tax Credits Before Filing

Tax deducted at source (TDS) and tax collected at source (TCS) play an important role in determining final tax liability and refunds. Errors in claiming tax credits can delay return processing. Taxpayers should confirm that all credits reflected in Form 26AS and related records match the amounts claimed in their returns. Reconciling these figures before submission can help prevent processing issues.

Correct Bank Details Are Essential for Refunds

Refund delays often occur because of incorrect banking information. Taxpayers should ensure that account numbers, IFSC codes and account validation requirements are accurate and up to date. Even if the return is processed successfully, incorrect bank details can prevent refunds from being credited on time.

Responding Quickly to Notices Matters

After filing an ITR, taxpayers should continue monitoring communications from the Income Tax Department. Notices seeking clarification, requests for additional information or defect intimations should not be ignored. Prompt responses can help resolve issues efficiently and reduce the chances of prolonged processing delays.

A Final Review Can Prevent Costly Errors

Before submitting a return, taxpayers should conduct a thorough review of all information, including income disclosures, deductions, tax credits and personal details. Cross-checking records against official tax documents can reduce the likelihood of mismatches and improve the chances of smooth processing. Spending a little extra time on verification can help avoid notices and ensure faster refund settlements.

Key Risks

- Income details may not match AIS, TIS or Form 26AS records.

- Unsupported deduction claims can attract verification notices.

- Unreported capital gains may lead to tax scrutiny.

- Incorrect bank details can delay refund credit.

Summary

Filing an accurate ITR for FY26 requires careful verification of income, deductions, investments and tax credits. As tax authorities increasingly rely on data-driven verification, discrepancies can result in notices or delayed refunds. Reviewing official tax records, reporting all income sources correctly and ensuring complete disclosures can help taxpayers avoid common filing mistakes and achieve smoother return processing.

FAQs

Q: What is the most common reason for receiving a tax notice after filing an ITR?

A: Income mismatches between the tax return and official records are among the most common triggers.

Q: Can missing interest income create problems during return processing?

A: Yes, omitted interest income may create discrepancies and lead to verification requests.

Q: Why is verifying bank account information important while filing an ITR?

A: Accurate bank details help ensure that any eligible refund is credited without delays.