AI-Led Revenue Expansion and Margin Strength Overshadowed by Weak Technical Sentiment

Shares of eClerx Services Limited (NSE:ECLERX) traded marginally lower in the latest session, trading near ₹1,511.90 despite reporting strong Q4FY26 and FY26 earnings growth driven by AI-powered analytics, automation services, and expanding enterprise demand.

The stock remains under pressure after failing to sustain above the 51-day EMA near ₹1,599, reflecting cautious investor sentiment amid broader weakness in the IT and digital transformation sector.

eClerx reported robust revenue growth, improving profitability, and continued client expansion during FY26, supported by strong demand from BFSI, communications, media, retail, and emerging verticals.

eClerx Reports Strong FY26 Revenue and Profit Growth

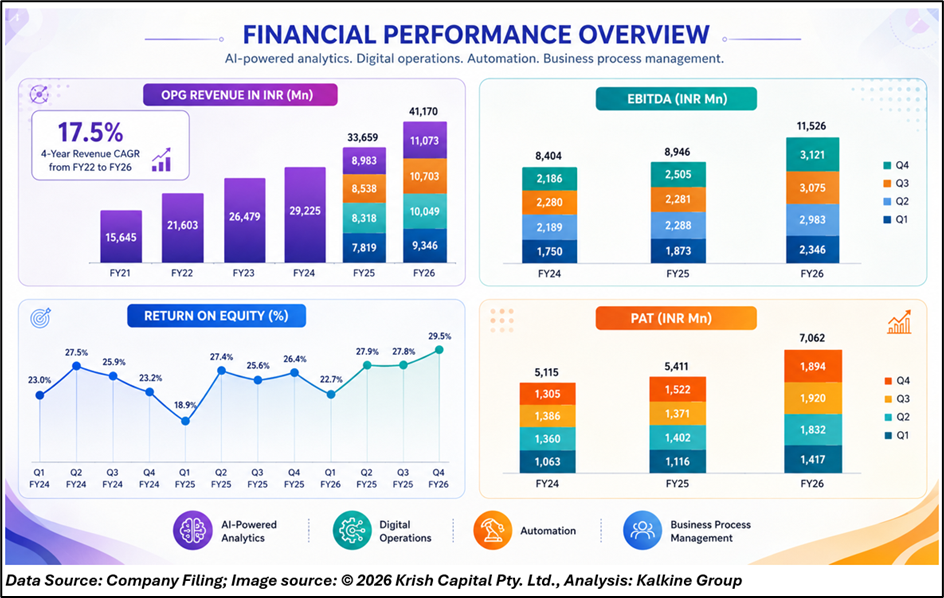

eClerx Services reported FY26 consolidated total revenue of ₹4,217 crore, registering 22.6% year-on-year growth, while operating revenue rose 22.3% to ₹4,117 crore. In dollar terms, operating revenue increased 17.9% year-on-year to US$468.9 million.

Profit after tax for FY26 climbed 30.5% year-on-year to ₹706 crore compared with ₹541 crore in FY25, while EBITDA increased 28.8% to ₹1,152 crore. EBITDA margin improved to 27.3% during FY26 from 26% in the previous year.

For Q4FY26, the company reported total revenue of ₹1,135 crore, up 23.9% year-on-year, while operating revenue rose 23.3% to ₹1,107 crore. Quarterly net profit stood at ₹189 crore despite a marginal sequential decline due to higher employee costs and investments in growth initiatives.

Management highlighted that constant currency revenue growth for FY26 stood at 17%, while Q4 constant currency growth remained positive at 0.5% quarter-on-quarter.

AI, Automation and Client Expansion Drive Growth

The company continued witnessing strong traction in AI-powered analytics, digital operations, and business process management solutions across global enterprises. eClerx added several large deals during FY26, with annual contract value momentum remaining healthy across strategic and emerging clients.

The BFSI segment remained the largest contributor with nearly 41% revenue share during FY26, followed by communications, media, and technology verticals. Emerging industries also continued gaining traction during the year.

North America contributed nearly 78% of revenue during Q4FY26, highlighting the company’s strong exposure to US enterprise spending trends. Client concentration also improved, with top-10 client contribution moderating to 59% from 64% a year earlier.

eClerx’s total headcount increased to over 22,600 employees during FY26, reflecting rising demand visibility and ongoing capacity expansion across offshore delivery centers.

Strong Cash Generation and Healthy Balance Sheet Support Outlook

The company maintained a strong balance sheet with cash and cash equivalents rising to ₹1,281 crore during FY26. Net operating cash flow also improved significantly to ₹873 crore, supporting future expansion and technology investments.

Management proposed a dividend of ₹1 per share for FY26 and also completed a 1:1 bonus issue during Q4FY26, reinforcing shareholder returns. Wage increments are scheduled to become effective from April 1, 2026, which may create short-term margin pressure but reflects confidence in long-term growth visibility.

The company’s increasing exposure to AI-driven operations, automation services, and digital transformation projects positions it favorably amid rising enterprise spending on operational efficiency and data analytics.

Technical Summary

eClerx stock remains weak after failing to sustain above the 51-day EMA near ₹1,599. The broader chart structure still reflects medium-term consolidation following a steep correction from previous highs near ₹2,400. RSI near 47 indicates neutral-to-weak momentum. Immediate support is visible near ₹1,450, while resistance remains around ₹1,620–1,650 levels.

Chart by TradingView

Conclusion

eClerx Services delivered strong FY26 financial performance driven by robust revenue growth, margin expansion, AI-led transformation demand, and improving deal momentum across global markets.

While near-term technical weakness and cautious IT sector sentiment continue limiting stock upside, the company’s strong cash generation, expanding client base, and growing digital operations business support long-term growth prospects.

FAQs

- Why did eClerx stock decline despite strong FY26 results?

The stock corrected due to weak technical sentiment, IT sector pressure, and profit booking after recent volatility.

- What was eClerx’s FY26 revenue growth?

eClerx reported 22.6% year-on-year growth in FY26 total revenue, reaching ₹4,217 crore.

- Which sectors contribute most to eClerx revenue?

BFSI remains the largest contributor, followed by communications, media, technology, retail, and emerging industry segments.