Shares of Chalet Hotels Limited (NSE:CHALET) gained nearly 3% in the latest trading session, with the stock currently trading near ₹774 after the company reported strong FY26 financial performance and announced multiple expansion initiatives across India’s premium hospitality market.

The hospitality major witnessed improved investor sentiment following robust earnings growth, rising average room rates, expansion in commercial real estate assets, and strategic additions to its luxury hotel pipeline. Despite broader volatility in hospitality stocks amid geopolitical disruptions impacting international travel, Chalet Hotels continued demonstrating operational resilience supported by strong domestic travel demand and premium positioning across key metro markets.

Chalet Hotels Reports Strong FY26 Revenue and Profit Growth

Chalet Hotels reported consolidated FY26 revenue of ₹28,124 million, reflecting sharp 60% year-on-year growth, while EBITDA increased 59% to ₹12,301 million. EBITDA margins stood at 43.7% during FY26, highlighting strong operational efficiency and improved business mix.

Excluding the residential business segment, FY26 revenue rose 18% year-on-year to ₹20,741 million, while EBITDA increased 21% to ₹9,573 million. The EBITDA margin for the core hospitality and commercial real estate business improved to 46.2%.

Profit after tax surged significantly to ₹6,450 million during FY26 compared with ₹1,425 million in FY25, supported by strong operating leverage and improved profitability across hospitality assets. Earnings per share also increased sharply to ₹29.50 from ₹6.53 in the previous year.

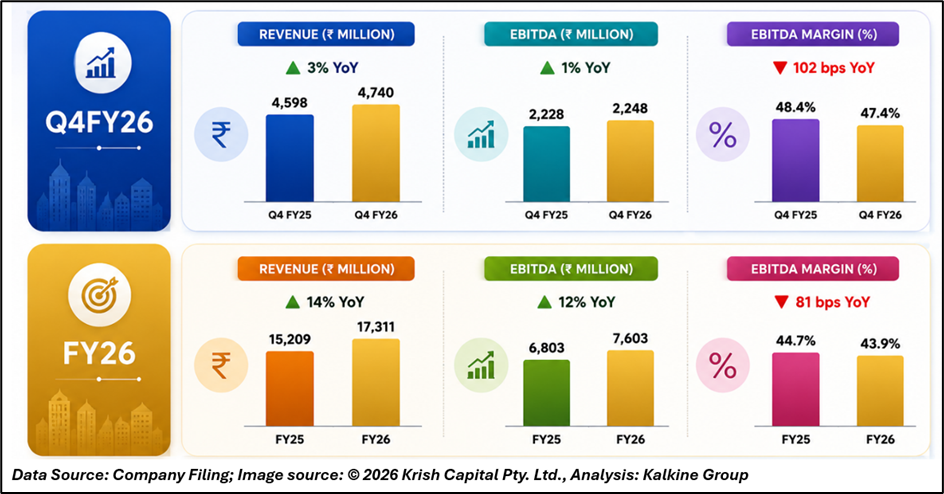

During Q4FY26, consolidated revenue rose 6% year-on-year to ₹5,711 million, while EBITDA increased 8% to ₹2,786 million. Quarterly PAT climbed 32% year-on-year to ₹1,630 million.

Hospitality Business Shows Pricing Strength Despite Occupancy Pressure

The company’s hospitality segment generated FY26 revenue of ₹17,311 million, reflecting 14% year-on-year growth, while EBITDA rose 12% to ₹7,603 million.

Average room rates across the hotel portfolio remained strong, with ADR increasing 7.7% year-on-year during Q4FY26 to ₹15,456. However, occupancy declined to 68.2% from 75.9% due to temporary disruptions linked to the West Asia geopolitical crisis and renovation activity across select Mumbai Metropolitan Region properties.

Management highlighted that occupancy in Bengaluru was impacted due to incremental room additions during FY26, while renovation and redevelopment work at select properties temporarily affected utilization levels. Nevertheless, premium leisure demand, corporate travel, and wedding-related bookings continued supporting overall business performance.

Expansion Pipeline Strengthens Long-Term Growth Outlook

Chalet Hotels continued expanding aggressively during FY26 through strategic acquisitions and greenfield developments.

The company acquired Inder Residency Resort & Spa in Udaipur for ₹1,710 million and plans to reposition the property into a premium luxury destination after renovation.

Additionally, Chalet announced development of an ultra-luxury Ritz-Carlton hotel project in Hyderabad comprising approximately 330 keys along with luxury retail space. The project is expected to launch by FY29 and is expected to significantly strengthen Chalet’s premium hospitality portfolio.

The company’s development pipeline now includes nearly 1,655 rooms and 0.9 million square feet of commercial real estate projects across Goa, Delhi NCR, Navi Mumbai, Hyderabad, and Kerala.

Chalet’s commercial real estate segment also delivered strong performance during FY26, with revenue increasing 55% year-on-year to ₹3,061 million and EBITDA rising 65% to ₹2,544 million. Occupancy across commercial assets remained healthy at 88%, supporting recurring annuity income visibility.

Technical Summary

Chalet Hotels stock is currently trading near ₹774 and remains slightly below its 51-day EMA near ₹779, indicating near-term consolidation after previous weakness. The broader structure suggests recovery attempts following correction from highs above ₹1,000. RSI near 51 reflects neutral momentum. Immediate support is visible near ₹740, while resistance remains around ₹800–820 levels.

Chart by TradingView

Conclusion

Chalet Hotels delivered strong FY26 operational and financial performance supported by premium pricing power, hospitality demand recovery, and expanding commercial real estate operations. Its aggressive luxury expansion strategy, growing annuity income, and strong development pipeline continue strengthening long-term growth visibility.

However, near-term occupancy disruptions and broader hospitality sector volatility may continue influencing short-term investor sentiment.

FAQs

- Why did Chalet Hotels shares rise recently?

The stock gained after strong FY26 earnings growth and announcement of multiple luxury expansion projects.

- What was Chalet Hotels’ FY26 revenue growth?

The company reported 60% year-on-year growth in consolidated FY26 revenue.

- What are Chalet Hotels’ major expansion plans?

The company is expanding through luxury hospitality projects in Hyderabad, Udaipur, Goa, Kerala, and Delhi NCR.