India’s hospitality sector could be entering another strong growth phase as slowing outbound travel and rising domestic tourism trends continue to support hotel demand across the country.

Indian Hotels Company Limited (NSE:INDHOTEL), the parent company of Taj Hotels, is increasingly focusing on India’s domestic travel opportunity amid global geopolitical disruptions and softer international travel activity.

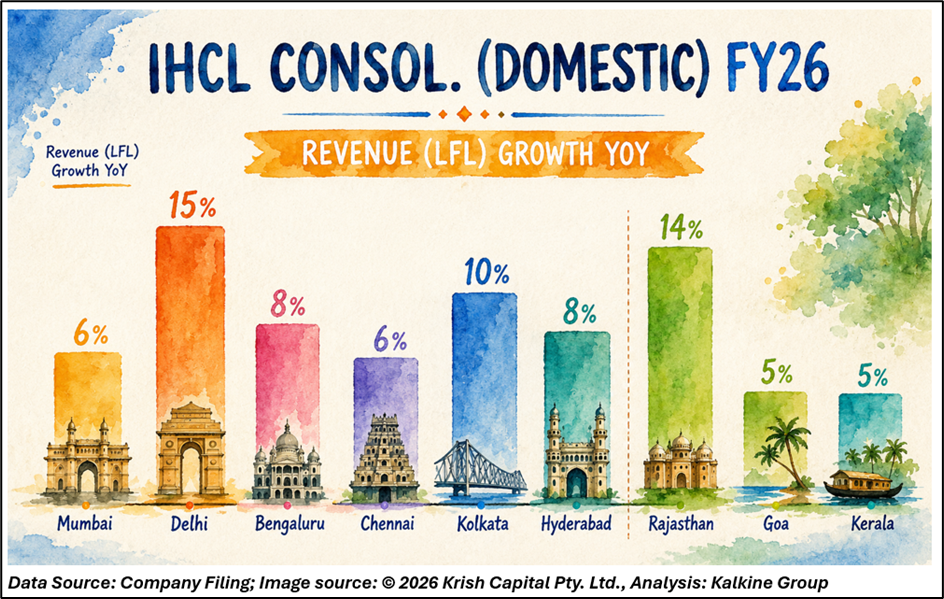

The company believes rising domestic tourism, weddings, leisure travel, religious tourism, and business events could help offset temporary weakness in inbound international travel.

Domestic Tourism Emerging as a Key Growth Engine

Recent geopolitical tensions in West Asia and disruptions in international air travel have affected global travel sentiment. However, India’s domestic hospitality demand has remained resilient, supported by strong leisure and business travel activity.

IHCL management highlighted that domestic tourism continued to power occupancy and revenue growth despite temporary disruptions in international travel routes and MICE-related cancellations.

The company also indicated that domestic demand remained structurally strong even as global disruptions impacted overseas travel trends.

Prime Minister Narendra Modi’s appeal encouraging citizens to prioritise domestic destinations over international travel may further support India’s hospitality and tourism ecosystem in the coming quarters.

IHCL Continues Strong Financial Momentum

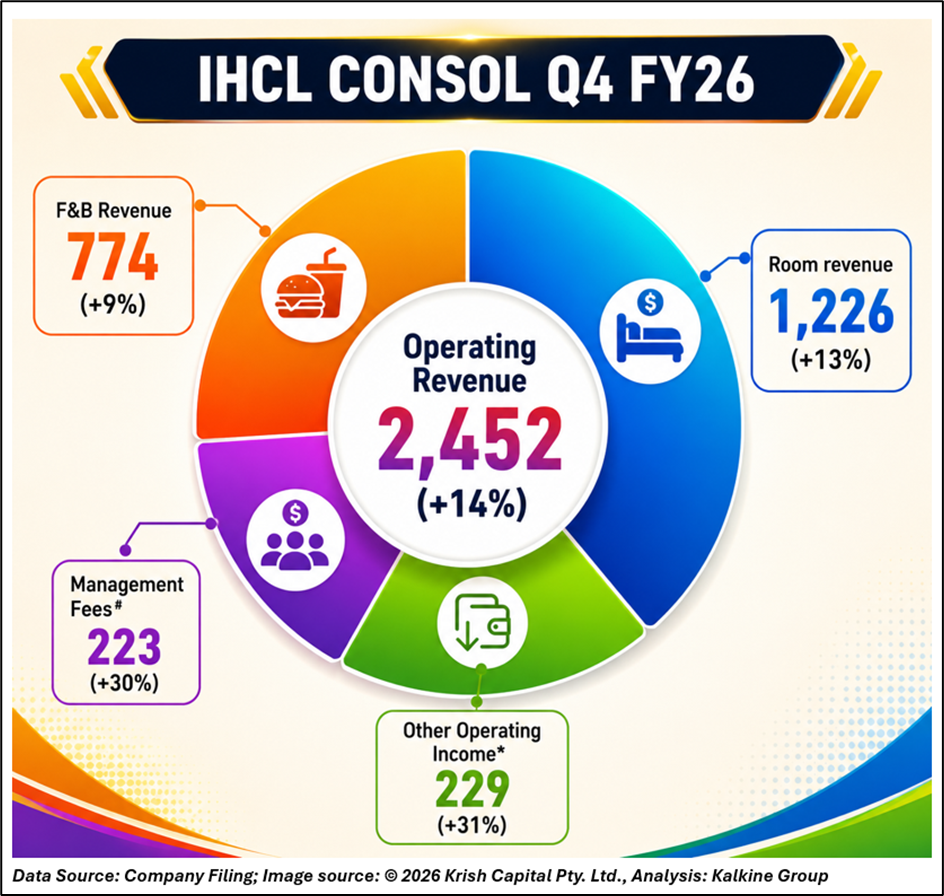

IHCL delivered another strong financial year despite geopolitical uncertainties and macroeconomic challenges.

According to the company’s FY26 investor presentation:

- Consolidated revenue rose 16% YoY to ₹9,971 crore

- EBITDA increased 16% to ₹3,477 crore

- PAT before exceptional items grew 15% to ₹1,849 crore

- EBITDA margin stood at 34.9%

The company described FY26 as its “best-ever financial performance” despite multiple external disruptions including geopolitical conflicts, heavy rains, flight cancellations, and travel uncertainties.

Revenue Per Room Growth Remains Strong

IHCL also reported healthy growth in RevPAR (Revenue Per Available Room), reflecting sustained pricing power and strong occupancy levels.

For FY26:

- IHCL consolidated RevPAR increased 9% YoY to ₹11,750 per night

- Occupancy remained strong at 76%

- Premium Taj properties continued to deliver strong pricing growth

The company’s premiumisation strategy and diversified brand portfolio continue supporting higher room realizations across luxury, upscale, and midscale segments.

Aggressive Expansion Across India

IHCL is accelerating its domestic expansion strategy to capitalise on India’s long-term tourism growth story.

As of April 2026, the company had:

- 630 hotels across brands

- 375 amã villas

- 1,000+ total portfolio units

- 255 hotels in pipeline

- Presence across 250+ destinations globally

The company expects over 60 hotel openings in FY27 and plans to further strengthen its presence across leisure, spiritual, and business destinations.

Weddings, Events and Tourism Driving Demand

IHCL expects multiple structural demand drivers to support the hospitality sector in FY27, including:

- Strong wedding season demand

- Major sporting events

- Large-scale business conferences and MICE activity

- Government-led tourism initiatives

- Rising discretionary spending among Indian consumers

The company also expects hotel supply to remain relatively tight across major Indian cities, which may support occupancy and pricing growth.

Capital-Light Strategy Supporting Growth

IHCL continues focusing on a capital-light expansion strategy through management contracts and partnerships.

The company stated that nearly 93% of its pipeline is capital-light in nature, helping improve scalability and return ratios.

Management fee income has also emerged as a major growth driver, rising 22% YoY in FY26.

Technical Summary

Indian Hotels Company is currently trading at ₹645.75 with a sideways-to-mildly positive bias. The stock remains around its 51-day EMA, indicating consolidation after a prolonged corrective phase. RSI near 50 reflects neutral momentum conditions. Sustained movement above ₹650–660 could improve near-term sentiment, while downside support is visible near ₹620 levels.

Chart by TradingView

Outlook

India’s hospitality sector appears well-positioned to benefit from the structural rise in domestic tourism, improving discretionary spending, and expanding travel infrastructure. With strong brand positioning, aggressive expansion, and resilient demand trends, IHCL could remain a key beneficiary of India’s long-term tourism growth story.

FAQs

- Why is IHCL focusing more on domestic tourism?

Domestic travel demand in India remains strong despite temporary weakness in international travel due to geopolitical disruptions.

- How did IHCL perform financially in FY26?

IHCL reported consolidated revenue of ₹9,971 crore and EBITDA of ₹3,477 crore during FY26.

- Which hotel stocks could benefit from rising domestic tourism?

Hospitality companies such as IHCL, EIH Hotels, Lemon Tree Hotels, Chalet Hotels, and Juniper Hotels may remain in focus.