Data Source: REFINITIV, Analysis: Kalkine Group

InterGlobe Aviation's sharp intraday rally signals more than a one-day trade — it reflects a structural repricing of India's dominant carrier as the ATF cost burden begins to meaningfully ease.

Key Highlights

- InterGlobe Aviation Ltd (NSE: INDIGO) surged +₹324.20 (+7.60%) to ₹4,593.20 on 8 April 2026, touching an intraday high of ₹4,744.00 — a move that briefly approached a near-10% intraday gain before a measured afternoon pullback.

- The rally is directly attributed to a sharp decline in crude oil prices, which carry immediate implications for Aviation Turbine Fuel (ATF) — IndiGo's single largest operating cost, representing approximately 35–40% of total airline operating expenses.

- IndiGo's latest earnings commentary confirmed ongoing cost discipline initiatives and yield improvement programs, creating a compounding earnings tailwind when combined with lower fuel costs.

- The stock opened at ₹4,600.00 against a previous close of ₹4,268.80 — a gap-up of ₹331.20 (7.76%) — reflecting overnight institutional positioning ahead of the crude-driven catalyst.

- With a market capitalisation of ₹1.78 lakh crore, IndiGo remains India's dominant listed aviation asset, and today's move reinforces its role as the primary vehicle for investors seeking exposure to India's structural aviation growth story.

Market Context: Why Aviation Is Moving Today

The economics of airline profitability are, in many ways, a function of one variable above all others: the price of jet fuel. Aviation Turbine Fuel — a kerosene-based derivative of crude oil — is not a cost that airlines can easily hedge away or substitute. It is a structural, recurring, and largely uncontrollable expense that determines the difference between margin expansion and margin compression in any given quarter.

When crude oil prices fall materially, the arithmetic for airline profitability changes rapidly and dramatically. A sustained 10% decline in ATF costs — all else being equal — can translate into hundreds of crores in annualised cost savings for an airline of IndiGo's scale. The market understands this transmission mechanism well, and today's 7.60% surge in INDIGO shares is a rational, forward-looking response to the improved cost outlook.

What makes the current move particularly significant is that it does not occur in isolation. IndiGo is not merely a passive beneficiary of falling crude prices. The company enters this favourable cost environment having already undertaken meaningful internal improvements — in yield management, network optimisation, and operational cost discipline — that amplify the earnings impact of any external tailwind. The combination of improving revenues and easing costs is the most powerful earnings upgrade catalyst available to an airline, and investors are pricing it in today.

Price Performance

Data Source: REFINITIV, Analysis: Kalkine Group

IndiGo's intraday price action on 8 April is textbook gap-up momentum. The stock opened at ₹4,600.00 — already well above the previous close of ₹4,268.80 — and extended gains to an intraday high of ₹4,744.00 within the first hour of trading. This early peak was followed by a gradual, orderly consolidation, with the stock settling around ₹4,593.20–₹4,620.00 through the mid-afternoon session.

The pattern is significant. An intraday chart that gaps up strongly, makes a new high early in the session, then consolidates — rather than selling off sharply — indicates genuine institutional accumulation rather than speculative retail momentum. Profit-taking at the highs was absorbed without breaking the stock back toward the gap-fill level, which speaks to the depth of buying interest at current prices.

The 52-week context is equally important. IndiGo's 52-week range spans ₹3,895.20 to ₹6,232.50 — a band of approximately 60% from low to high. At ₹4,593.20, the stock sits roughly in the middle of this range, closer to its lows than its highs. This positioning suggests that despite today's strong move, the stock remains meaningfully below the valuations investors were willing to assign it at peak sentiment — implying substantial recovery potential if the fundamental earnings upgrade story plays out over the next two to three quarters.

The distance from current price to the 52-week high of ₹6,232.50 represents approximately 35.7% upside — a recovery that would require sustained ATF cost relief, continued yield improvement, and credible capacity growth execution. It is not a foregone conclusion, but it is a realistic medium-term scenario if management delivers on its stated strategic priorities.

Technical Analysis

IndiGo's intraday chart on 8 April presents a constructive technical picture, with several key observations for investors and traders:

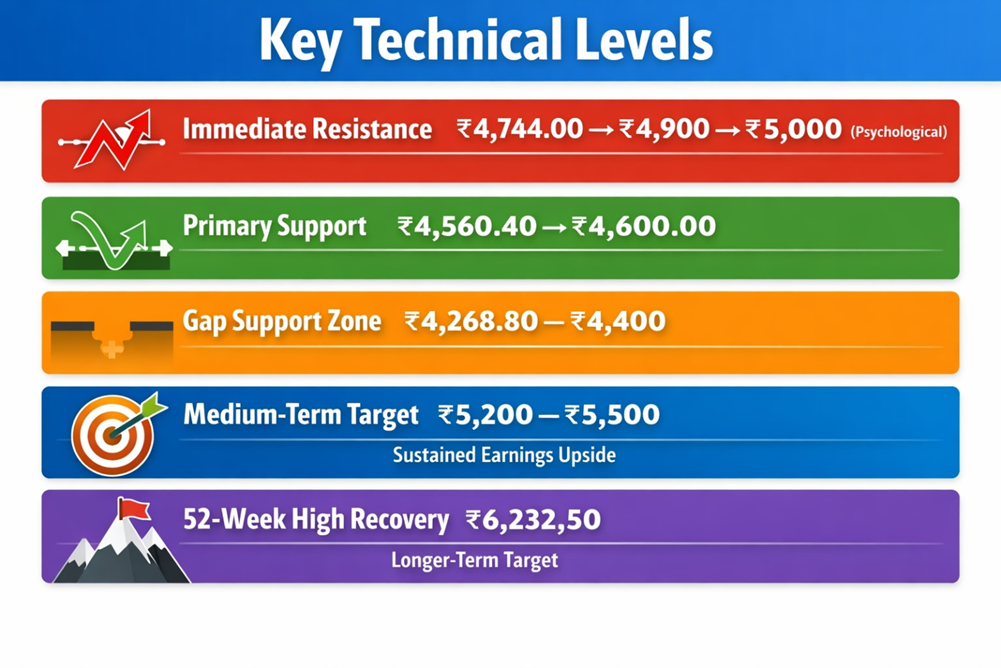

Gap-Up Structure: The gap between the previous close (₹4,268.80) and today's open (₹4,600.00) creates a significant support zone in the ₹4,268–₹4,400 range. Gap-fill moves are common in the days following strong gap-up sessions; a pullback to this zone — should it occur — would represent a technically attractive re-entry level for investors who missed today's move.

Intraday High as Near-Term Resistance: ₹4,744.00 — today's high — becomes the immediate resistance level. A sustained close above this level on volume would signal continuation of the uptrend and open the path toward the ₹4,900–₹5,000 psychological range.

Key Technical Levels:

Data Source: REFINITIV, Analysis: Kalkine Group

Momentum Indicators: The strength of today's move — 7.60% on what appears to be elevated volume — is consistent with a momentum signal that technical traders will interpret as a trend resumption rather than a one-day event. The stock had been consolidating above its 52-week low of ₹3,895.20, and today's breakout above ₹4,500 is technically meaningful.

Risk Consideration: The primary technical risk is a crude oil price reversal. If oil prices recover sharply in the coming sessions, IndiGo could retrace a significant portion of today's gains. Investors should be aware that the stock's near-term trajectory is highly correlated with crude oil price movements.

Financial Update — Recent Filing and Earnings Commentary

Based on IndiGo's latest earnings commentary and publicly available disclosures:

Cost Structure: ATF accounts for approximately 35–40% of IndiGo's total operating costs — the single largest expense line and the most volatile. At IndiGo's scale of operations, even a modest percentage decline in ATF prices translates into substantial absolute cost savings. A 10% decline in jet fuel prices, sustained over a full financial year, could add several hundred basis points to operating margins.

Cost Discipline Initiatives: Management's latest earnings commentary explicitly highlighted ongoing cost discipline across the business — encompassing aircraft utilisation optimisation, maintenance cost management, ground handling efficiency, and overhead rationalisation. These internal measures reduce the company's breakeven load factor and improve its ability to generate positive operating cash flow across a wider range of demand scenarios.

Yield Improvement: IndiGo's management has flagged active yield management initiatives — including dynamic pricing optimisation, ancillary revenue development, and network rationalisation toward higher-yielding routes. Yield improvement is a revenue-side lever that operates independently of fuel costs, and when both improvements occur simultaneously, the earnings impact is multiplicative rather than additive.

Capacity Outlook: IndiGo continues to expand its fleet and route network, leveraging its dominant domestic market position to grow both absolute passenger volumes and revenue per available seat kilometre (RASK). Capacity discipline — adding seats where yields are strong, pulling back where they are not — has been a hallmark of the current management team's approach.

Dividend Policy: The quarterly dividend of ₹2.53 per share (yield: 0.22%) reflects IndiGo's primary allocation of capital toward fleet expansion and operational investment rather than near-term shareholder distributions — a rational choice for a growth-phase aviation business operating in one of the world's fastest-growing aviation markets.

Management Outlook

IndiGo's management enters the current operating environment with a constructive medium-term narrative supported by both structural and cyclical tailwinds.

Structural tailwind: India's domestic aviation market is one of the fastest-growing in the world, underpinned by rising middle-class incomes, increasing propensity to fly, and significant infrastructure investment in airport capacity. IndiGo, with its dominant market share — consistently above 55% of domestic passenger traffic — is the primary beneficiary of this growth.

Cyclical tailwind: The current decline in crude oil prices provides a direct and immediate margin improvement opportunity. Management's stated approach of combining external cost relief with internal efficiency gains reflects a disciplined operational philosophy that has been the foundation of IndiGo's long-term competitive advantage.

Fleet Management: The resolution of engine supply constraints that weighed on capacity deployment in prior periods has been a key management focus. Progress on normalising aircraft availability directly impacts IndiGo's ability to capture peak-season demand — a particularly important consideration heading into the summer travel season.

International Expansion: Management has indicated continued focus on expanding IndiGo's international network, targeting both short-haul South and Southeast Asian routes and medium-haul Middle Eastern corridors. International yield dynamics tend to be more favourable than domestic routes, making this expansion a margin-accretive growth vector if executed successfully.

Guidance Risk: Aviation management outlooks are inherently sensitive to exogenous variables — crude prices, weather events, geopolitical disruptions, and regulatory changes. Investors should treat any forward guidance from airline management as indicative rather than definitive.

Frequently Asked Questions (FAQs)

Q: Why did IndiGo's stock jump so sharply today?

The primary catalyst was a significant decline in crude oil prices, which directly reduces Aviation Turbine Fuel (ATF) costs — IndiGo's largest operating expense at 35–40% of total costs. Combined with positive internal developments around cost discipline and yield improvement, the market repriced the stock sharply higher to reflect improved earnings visibility.

Q: Is a 7.60% single-day gain sustainable for IndiGo?

Single-day moves of this magnitude in airline stocks typically reflect a genuine fundamental catalyst — in this case, a meaningful crude oil price decline — rather than pure speculation. Sustainability depends on whether crude prices remain subdued. If they do, the earnings upgrade cycle is likely to persist, supporting the stock at current or higher levels.

Q: What is ATF and why does it matter so much for IndiGo?

Aviation Turbine Fuel is the jet fuel used by commercial aircraft. It is a crude oil derivative and typically represents 35–40% of an airline's total operating costs. Because it cannot be substituted and is difficult to fully hedge, movements in crude oil prices directly and materially affect airline profitability.

Q: At ₹4,593, is IndiGo still attractive versus its 52-week high of ₹6,232.50?

The stock trades approximately 26% below its 52-week high, which implies meaningful recovery potential if the earnings upgrade thesis plays out. However, investors should note that the 52-week high was achieved under a specific set of market conditions, and recovery to those levels requires sustained execution on both cost management and revenue growth.

Q: What are the key risks to IndiGo's investment case?

The primary risks are a reversal in crude oil prices, weaker-than-expected domestic demand, any resurgence of aircraft availability constraints, and competitive intensity in the Indian aviation market. Currency risk — IndiGo's aircraft leases and some costs are denominated in USD — is also a persistent consideration.