Digital assets such as cryptocurrencies have gained attention among investors worldwide, including in India. While traditional retirement portfolios typically focus on fixed-income instruments, equities, and government-backed schemes, digital assets are increasingly being discussed as a supplementary investment option. However, due to their volatility and evolving regulatory environment, digital assets require careful evaluation before inclusion in retirement planning. The global discussion around cryptocurrency highlights its diversification potential but also emphasizes significant volatility and regulatory risks that must be considered in long-term portfolios.

Understanding Digital Assets in the Indian Context

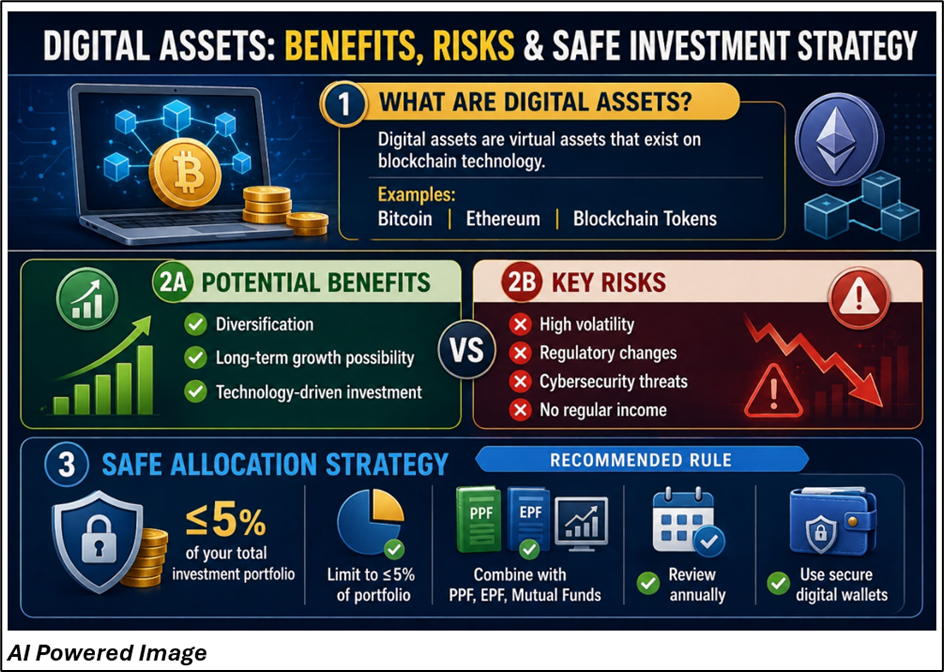

Digital assets refer primarily to cryptocurrencies such as Bitcoin and Ethereum, along with blockchain-based tokens. In India, cryptocurrencies are not considered legal tender but are permitted as digital assets under regulatory frameworks, with taxation rules currently applied on gains.

For retirement planning, digital assets should not replace traditional investments but may be evaluated as a small component within a diversified portfolio.

Key characteristics of digital assets include:

- High price volatility

- Limited long-term historical data

- Technology-driven value

- Market sentiment-based pricing

- Regulatory uncertainty

These features make digital assets fundamentally different from stable retirement instruments such as PPF, EPF, or Senior Citizens’ Savings Scheme (SCSS).

Why Digital Assets Are Considered in Retirement Planning

Despite the risks, some investors consider digital assets for specific reasons.

- Portfolio Diversification- Digital assets often behave differently from traditional investments like stocks or bonds. This difference may provide diversification benefits under certain market conditions. However, diversification does not guarantee protection against losses, and correlations between asset classes can change over time.

- Potential for Long-Term Growth- Cryptocurrencies are often associated with technological innovation and digital adoption. Some investors believe they offer long-term growth potential due to increasing global usage of blockchain technology. However, retirement portfolios should not rely on uncertain returns from high-risk assets.

- Hedge Against Currency Depreciation (Debated)- Certain cryptocurrencies have limited supply mechanisms, leading to discussions about their role as potential inflation hedges. However, this concept remains debated, and digital assets should not be viewed as guaranteed protection against inflation.

- Risks of Including Digital Assets in Retirement Portfolios Digital assets present several risks that must be considered carefully, especially for retirement planning.

- Price Volatility- Cryptocurrency prices can fluctuate significantly within short periods. This volatility can affect retirement portfolio stability and increase financial risk.

- Regulatory and Taxation Risks- India’s cryptocurrency regulations are still evolving. Changes in taxation or policy can impact asset valuation and liquidity. Currently, cryptocurrency gains are taxed under specific provisions, and transaction rules may change over time.

- Security and Custody Risks- Digital assets require secure storage solutions such as digital wallets. Loss of access credentials or cyber incidents can lead to permanent loss of funds. Retirement investors should prioritize security measures and reliable custodians.

- Lack of Regular Income- Unlike bonds or dividend-paying stocks, most cryptocurrencies do not generate regular income. This makes them less suitable for retirees who depend on predictable income streams.

Recommended Allocation Approach for Indian Investors

Financial planners typically suggest that digital assets, if included, should represent only a small portion of a retirement portfolio.

General allocation principles include:

- Limit exposure to 5% or less of total portfolio value

- Combine digital assets with traditional investments

- Review allocation periodically

- Avoid using retirement emergency funds for high-risk assets

These practices help manage volatility and protect retirement savings.

Governance and Monitoring of Digital Asset Investments

Including digital assets in retirement portfolios requires disciplined monitoring.

Investors should:

- Maintain clear allocation limits

- Track regulatory updates in India

- Conduct periodic portfolio rebalancing

- Maintain secure wallet practices

Without ongoing oversight, portfolio risk levels can increase unexpectedly.

Conclusion

Digital assets are an emerging component in modern investment discussions, but their role in Indian retirement portfolios remains supplementary rather than primary. While they may offer diversification and growth potential, their volatility, regulatory uncertainty, and security risks make cautious allocation essential. A well-balanced retirement strategy should prioritize stability, income generation, and long-term financial security before considering exposure to digital assets.

FAQs

- Are cryptocurrencies suitable for retirement planning in India?

Cryptocurrencies may be considered as a small supplementary investment but should not replace traditional retirement assets. - What percentage of retirement savings should be invested in digital assets?

Financial planners generally recommend limiting digital asset exposure to around 5% or less of total retirement investments. - What are the main risks of investing in cryptocurrencies for retirement?

Major risks include price volatility, regulatory changes, security threats, and lack of regular income generation.