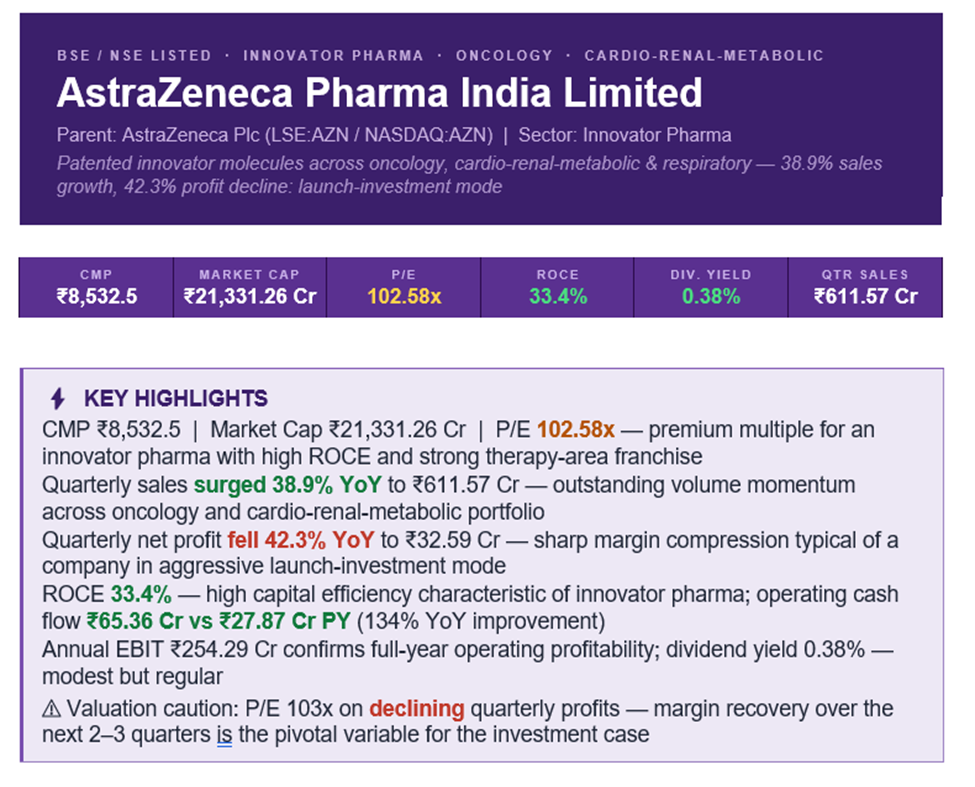

Key Financial Metric Dashboard:

Source: company BSE/NSE filings. Verify at bseindia.com and nseindia.com

Company Overview

AstraZeneca Pharma India Limited (BSE/NSE:ASTRAZEN) is the Indian listed subsidiary of AstraZeneca Plc, the UK-Swedish biopharmaceutical major and one of the world's leading innovator pharmaceutical companies. The Indian arm imports, markets, and distributes AstraZeneca's global portfolio of patented and off-patent medicines across oncology, cardiovascular, renal, metabolic, respiratory, and rare-disease therapy areas. Unlike Indian generic pharma majors that compete on cost and scale, AstraZeneca Pharma India operates an innovator-led model: launching globally validated, patent-protected molecules and capturing premium pricing in tertiary-care channels.

The Indian innovator pharma opportunity has expanded materially in the past decade. Rising household incomes, growing private health insurance, the build-out of corporate hospital chains, and increasing willingness to pay for branded specialty therapies have created a meaningful market. AstraZeneca's globally franchised drugs — including Tagrisso (lung cancer), Forxiga/Dapagliflozin (diabetes/cardio-renal), Brilinta (acute coronary syndrome), Symbicort (respiratory), and Lynparza (oncology) — are central to the Indian growth story.

Therapy Portfolio, Pipeline & Revenue Architecture:

Patent status and indications based on publicly available regulatory and company information. Verify current approval status from CDSCO (cdsco.gov.in). This is not promotional content for any medicine.

Financial Performance & Insights

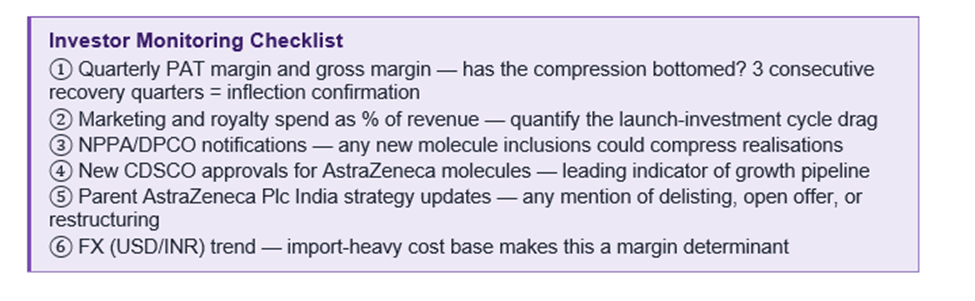

The latest quarter presents a divergent picture. Sales of ₹611.57 crore grew 38.9% YoY — an outstanding print indicating strong volume growth across the portfolio, plausibly led by oncology and cardio-renal-metabolic franchises where AstraZeneca's market share is rising. However, net profit fell 42.3% to ₹32.59 crore, signalling sharp margin compression. Possible drivers include higher import costs, FX translation impact, increased royalty or marketing spend behind new launches, and product-mix shifts towards lower-margin volumes.

This kind of decoupling — strong revenue, weak margins — is typical of an MNC pharma in launch-investment mode. Marketing, medical-affairs, and field-force spend front-load while volume gains take quarters to mature into operating leverage. The improvement in operating cash flow (₹65.36 Cr vs ₹27.87 Cr — a 134% jump) suggests working-capital discipline has improved significantly even as P&L margins compressed.

Annual EBIT of ₹254.29 crore confirms meaningful full-year operating profitability. ROCE of 33.4% confirms structural capital efficiency and earns the franchise its premium multiple. The next two to three quarters will determine whether the margin compression is a temporary investment phase or a structural reset — this is the single most important financial variable for investors at current levels.

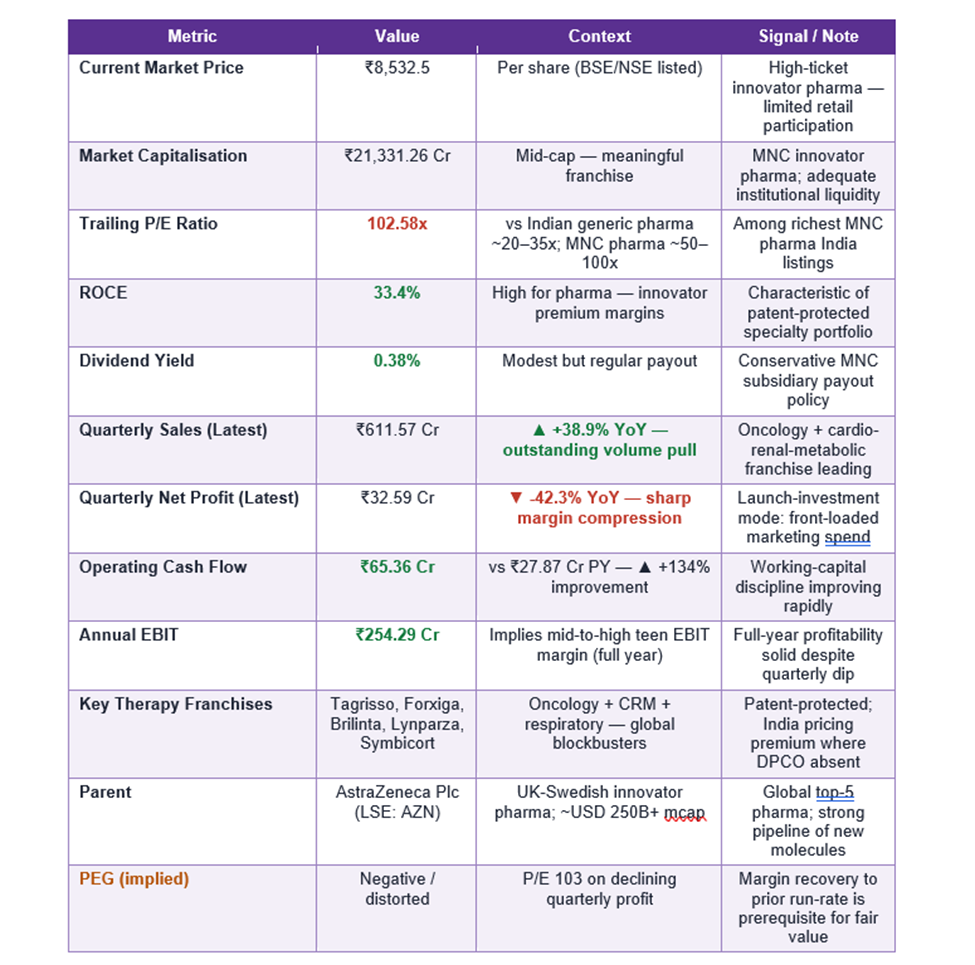

Financial Performance & Risk Scorecard:

Risk ratings are qualitative assessments based on BSE/NSE filings, and sector analysis.

Price Performance

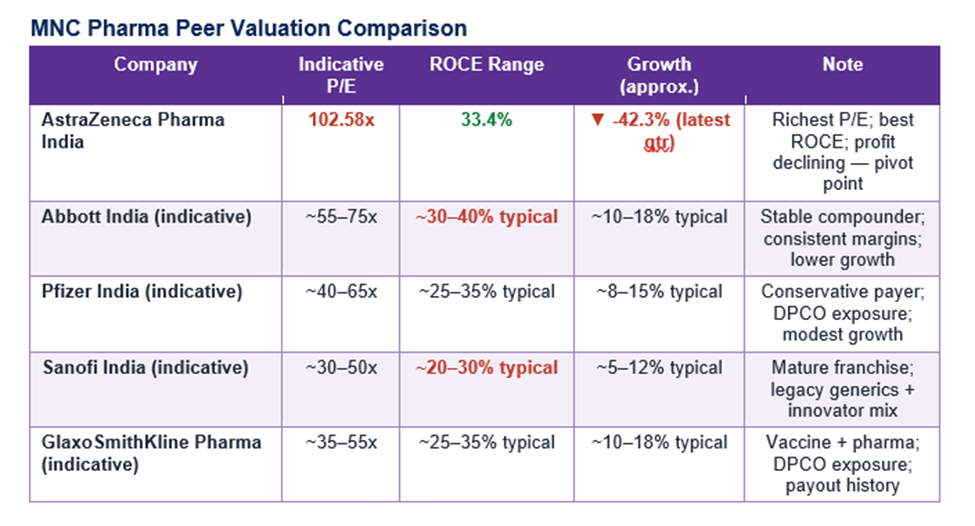

AstraZeneca Pharma India trades at ₹8,532.5, near the higher end of its historical price range. The stock has rerated meaningfully as investors have come to appreciate the durability of its specialty franchise and the launch cadence of new molecules. Multinational pharma listings in India — a small set including AstraZeneca, Pfizer, Sanofi India, Abbott India, and GlaxoSmithKline Pharma — typically trade at premium multiples reflecting their innovator portfolios.

Near-term price action will be sensitive to quarterly margins, which have come under pressure in the latest print, and to the timing of new launches and regulatory clearances. Investors should expect higher volatility around results and around any news flow on parental strategic decisions involving the Indian subsidiary.

Valuation

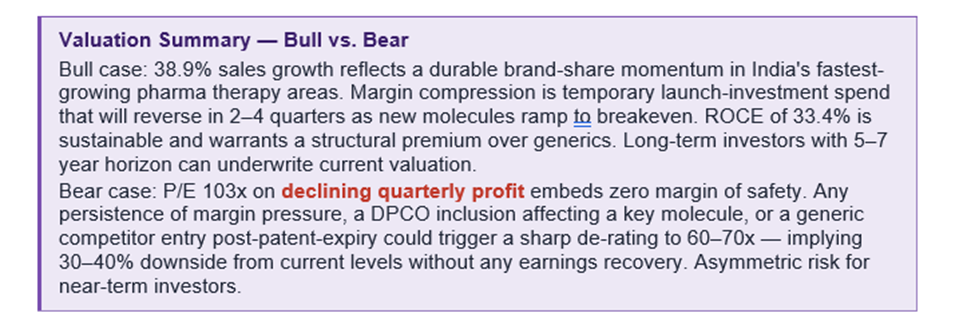

At a P/E of 102.58x and a market cap of ₹21,331 crore, the stock embeds two assumptions: that the current margin pressure is transitory, and that revenue growth at recent run-rates can be sustained for years. If both hold, the multiple becomes reasonable as forward earnings recover — the stock can grow into its valuation without re-rating. If margin pressure persists or revenue growth slows, the multiple is exposed to meaningful compression.

Peer P/E and ROCE ranges are indicative from sector data and publicly available data

Shareholder Returns & Dividend Policy

The company offers a 0.38% dividend yield. For a multinational subsidiary, the payout policy is typically conservative, with the bulk of earnings retained for working capital, marketing investment behind new launches, and royalty payments to the parent. Long-term shareholder returns have come overwhelmingly from share-price appreciation rather than dividends.

Long-term shareholders should evaluate total return through the lens of book-value compounding and earnings growth rather than current income. A future shift to a modest payout increase would be a positive signal that the parent considers the Indian entity to have crossed a maturity threshold.

Business Strategy & Outlook

Strategy rests on four pillars. First, accelerate launches of globally proven new molecules — particularly in oncology, where India's diagnosed-patient pool is expanding rapidly and willingness to pay for targeted therapies is rising. Second, deepen penetration of the cardio-renal-metabolic franchise (Forxiga and adjacencies), where India's diabetes and chronic kidney disease epidemiology supports multi-year volume growth.

Third, expand reach beyond metro tertiary hospitals into Tier-2 and Tier-3 cities through partnerships, digital-detailing, and patient-support programmes. Fourth, manage the regulatory and pricing environment proactively to preserve premium-pricing realisation where DPCO does not apply.

The 38.9% sales surge confirms the launch and detailing engine is working. The margin compression suggests a significant marketing-investment cycle is underway. The combination is consistent with a deliberate land-grab in fast-growing therapy areas — a reasonable strategy if investors are willing to underwrite the medium-term margin recovery.

Key Risks

1 — Valuation and Margin Recovery Risk (Primary)

At P/E 102.58 with profit declining 42.3%, the stock is priced for aggressive margin recovery. If cost pressures persist for several more quarters, the multiple will compress. Investors should stress-test the position against a scenario where margins recover only partially, arriving at 60–70x P/E — the level at which most MNC pharma peers trade — which implies 30–40% downside from current levels.

2 — Regulatory / DPCO Price Control

Drug-price control under DPCO and NPPA caps pricing for scheduled formulations. The inclusion list expands periodically and unpredictably. Several AstraZeneca molecules in high-volume therapeutic classes (diabetes, cardiovascular) could be brought under price control, compressing realisations.

3 — Other Risks

- Patent expiry: Key franchises losing patent protection in India trigger generic competition and price erosion. Tracking the patent cliff calendar is essential.

- FX and import dependency: A large share of finished products and APIs are imported from parent operations, exposing margins to rupee depreciation.

- Parent strategic risk: Royalty, pricing, technology fees, and subsidiary strategy are determined at parent level. Delisting attempts or open offers are not predictable.

- Related-party transactions: Royalty and intercompany sales terms warrant ongoing review — verify in annual report each year.

- Specialty channel concentration: Reliance on tertiary hospitals and oncologists creates customer concentration risk.

Frequently Asked Questions

Q1. What does AstraZeneca Pharma India do?

It is the Indian listed arm of UK-Swedish innovator pharma major AstraZeneca Plc, marketing patented and branded molecules across oncology, cardio-renal-metabolic, respiratory, and rare disease therapy areas in India.

Q2. Why did profit fall 42% despite 39% sales growth?

Margin compression from higher import/input costs, marketing investment behind new launches, FX impact, and unfavourable mix during a period of aggressive volume expansion. This pattern is typical of an MNC pharma in launch-investment mode — revenues front-run margins.

Q3. Is the dividend reliable?

A modest 0.38% yield is paid. Multinational subsidiaries typically maintain conservative payouts, prioritising reinvestment and parent-aligned capital choices. Long-term returns have come primarily from share-price appreciation.

Q4. What are the most important risks?

High P/E (103x) with falling profit, regulatory price control (DPCO/NPPA), import dependency and FX, parent-company strategic decisions (including potential delisting or royalty changes), related-party transactions, patent expiries, and specialty channel concentration.

Q5. How does it compare to other MNC pharma listings?

It trades at the higher end of the MNC pharma cohort (Pfizer India, Sanofi India, Abbott India, GSK Pharma) given its oncology and cardio-renal-metabolic franchise strength and 33.4% ROCE. The premium is directionally justified but leaves no room for execution slippage at current multiple levels.

Q6. What would make the bull case work?

Two to three consecutive quarters of PAT margin recovery back toward historical levels, confirmation that the launch-investment cycle is generating durable market-share gains in oncology and SGLT2 markets, no adverse DPCO inclusions, and stable to improving FX. If all three hold, the stock can grow into its multiple without further re-rating.