Source: Company BSE/NSE filings.

Company Overview

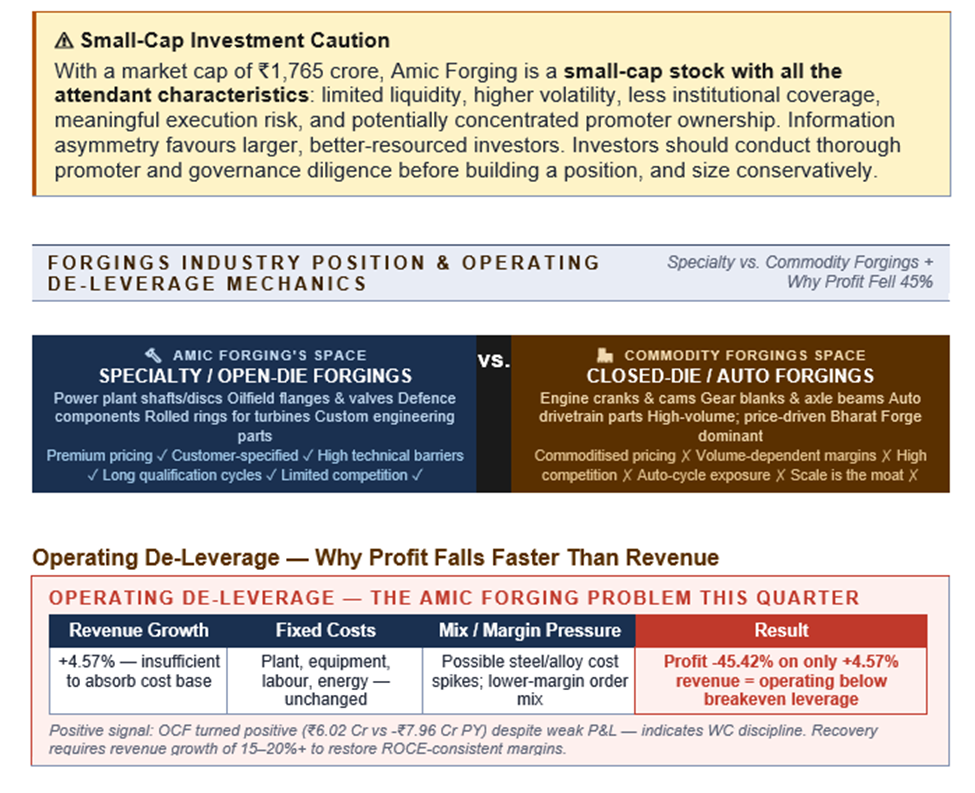

Amic Forging Limited (BSE:AMIC) is a specialty forgings manufacturer producing open-die forgings and rolled rings for industrial customers across power generation, oil and gas, defence, cement, steel, and general engineering. The company occupies a niche in the Indian forgings industry: open-die forgings are technically demanding, customer-specified products with relatively limited domestic competition, in contrast to the more commoditised closed-die forgings space dominated by automotive supply chains.

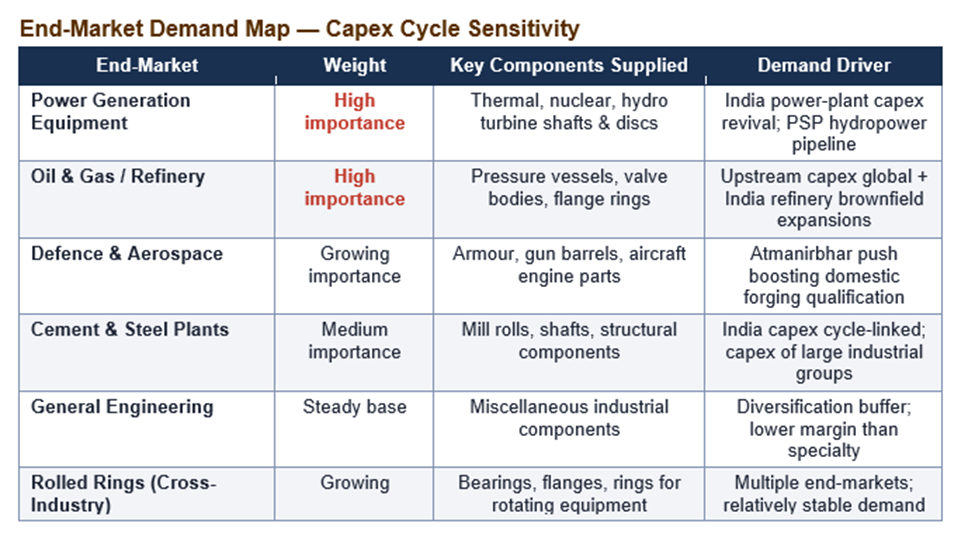

The forgings industry in India sits at the intersection of multiple capex-driven demand pools. Power-generation equipment, oilfield equipment, defence platforms, capital goods, and process industries all require large forged components — shafts, discs, rings, blocks — that smaller forgings shops cannot make. Players with the press capacity, heat-treatment infrastructure, and quality systems to serve these customers earn premium pricing and benefit from long-tenor relationships.

Financial Performance & Insights

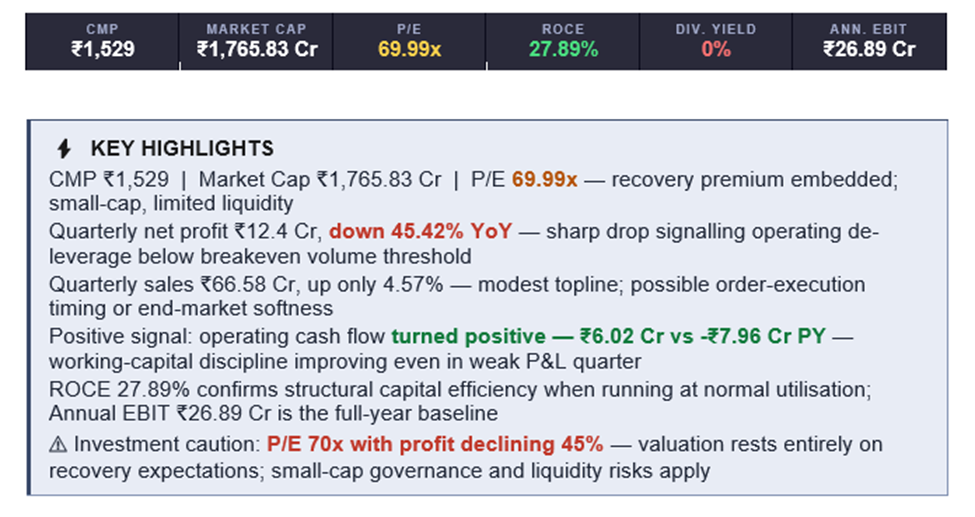

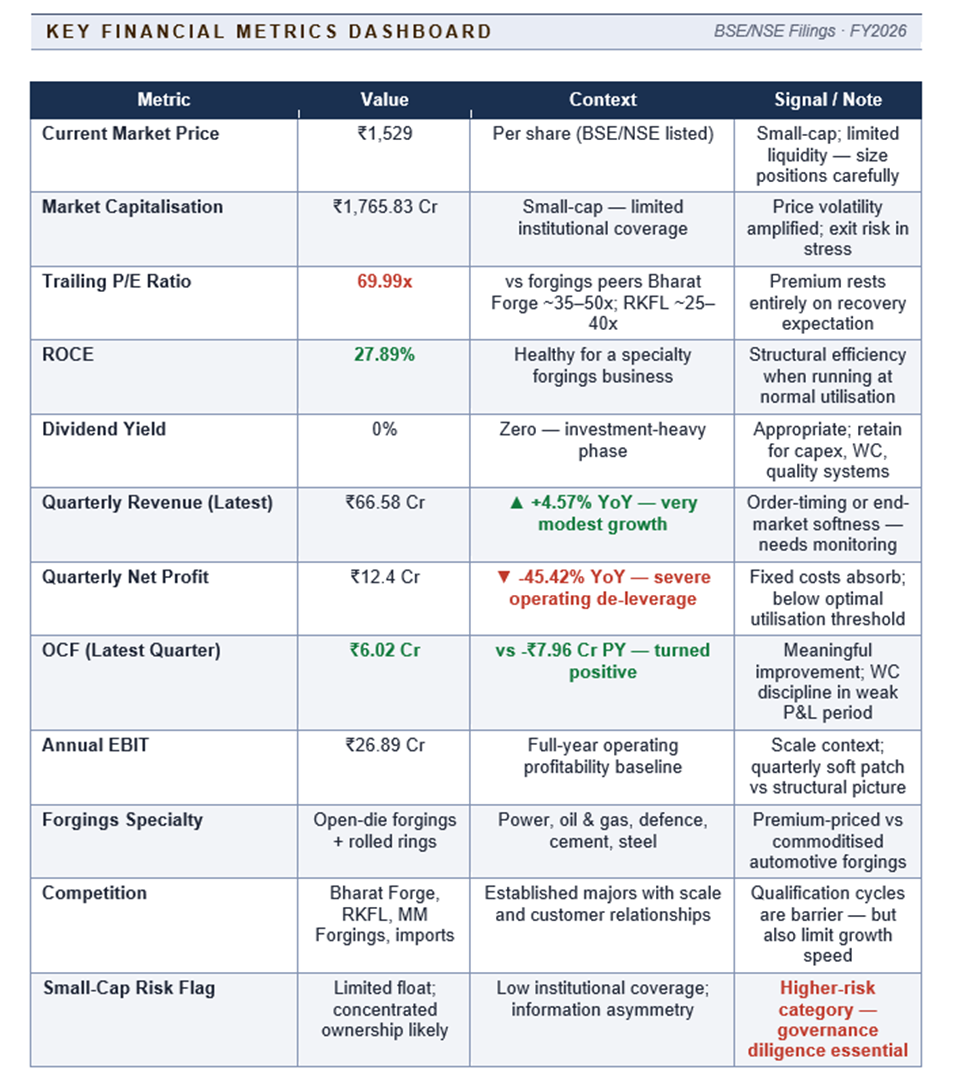

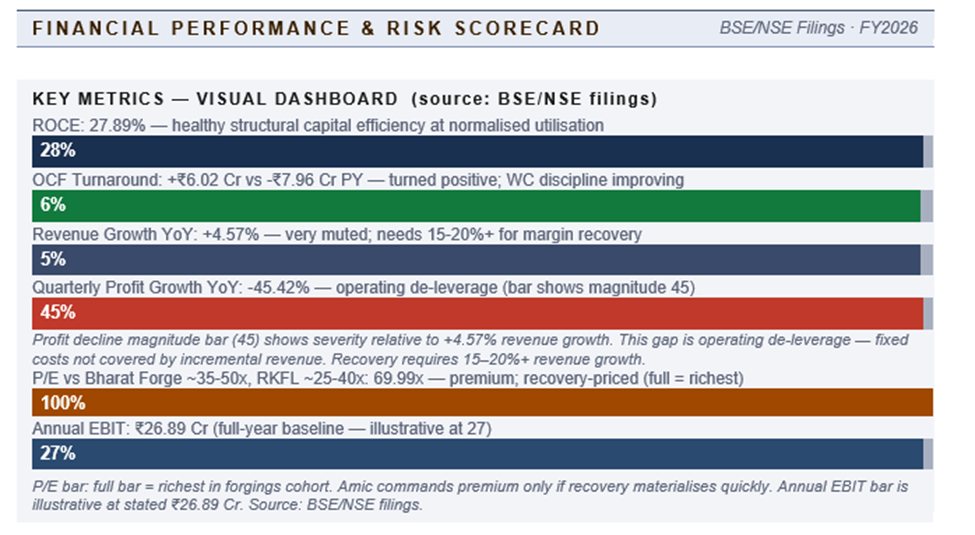

The latest quarter is a difficult print. Revenue of ₹66.58 crore grew only 4.57% YoY — a sharp deceleration suggesting either order-execution timing issues, customer-specific delays, or weakness in particular end-markets. Net profit of ₹12.4 crore fell 45.42% — a much sharper drop than the topline implies, pointing to significant operating de-leverage. Possible drivers include unfavourable product mix, raw-material cost pressure (steel prices and alloying elements), inventory write-downs, or higher fixed costs without commensurate volumes.

The one bright spot: operating cash flow turned positive at ₹6.02 crore versus negative ₹7.96 crore in the prior year. For a small forgings business this is meaningful — it suggests working capital is being managed better even during a soft P&L quarter. ROCE of 27.89% remains healthy and confirms the business is structurally capital-efficient when running at normal utilisation.

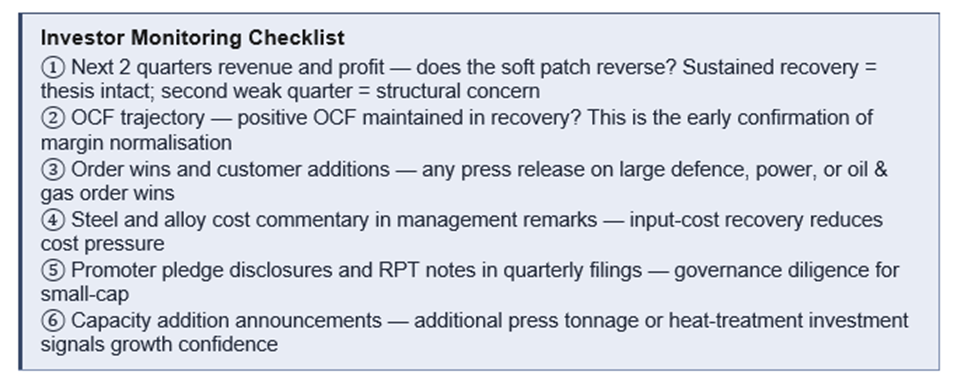

For investors, the read-through is mixed: the quarter is poor, but the cash-flow turnaround and structural ROCE leave open the possibility that this is a temporary execution issue rather than a structural deterioration. Two consecutive quarters will determine whether this is a soft patch or something more concerning.

Risk ratings are qualitative assessments based on BSE/NSE filings.

Price Performance

Amic Forging trades at ₹1,529, with the small-cap status creating amplified price action relative to fundamentals. Smaller forgings names have participated in the broader capital-goods rerating, with investors searching for under-followed plays on the capex theme. The stock's volatility reflects both this enthusiasm and the inherent characteristics of a small-cap with concentrated ownership and limited float.

The latest quarterly print — sharp profit decline — will be a near-term overhang. Recovery in price action is likely to require either a strong subsequent quarter, a meaningful order announcement, or broader small-cap risk-on conditions.

Shareholder Returns & Capital Allocation

Amic Forging pays no dividend. As a small-cap in an investment-heavy industry, retaining earnings to fund capacity, working capital, and product-quality investments is appropriate. Long-term shareholder returns will come from capital appreciation, conditional on continued growth, margin recovery, and successful capacity utilisation. Investors should not expect dividend income from this name in the near to medium term.

Key Risks

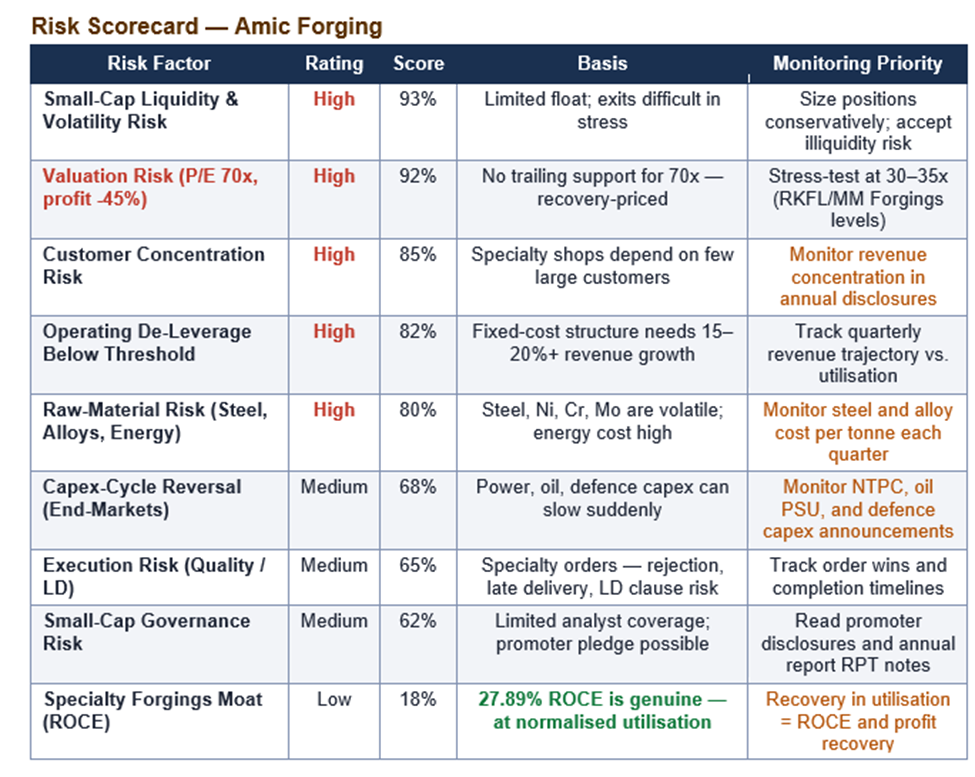

1 — Small-Cap Risk (Dominant)

Small-cap risk is the dominant concern. With a market cap of ₹1,765 crore and limited institutional coverage, price volatility is high, exits can be difficult during stress, and information asymmetry favours larger, better-resourced investors. Concentrated ownership can mean float is thin and bid-ask spreads wide. Investors should conduct full promoter and governance diligence before entry.

2 — Valuation Risk at 70x P/E

At 70x P/E with profit declining 45%, the multiple is supported only by the assumption of recovery. If recovery is delayed, multiple compression can be severe.

3 — Other Risks

- Customer concentration: Specialty-forgings shops depend on a handful of large customers; loss of any one creates immediate revenue gaps.

- Operating de-leverage: The business needs 15–20%+ revenue growth to absorb its fixed-cost structure; below that threshold, profits collapse disproportionately.

- Raw-material risk: Steel prices, alloying elements (nickel, chromium, molybdenum), and energy costs drive cost structure; spikes compress margins before pass-through.

- Execution risk: Quality rejections, late delivery, and liquidated damages on specialty orders can produce idiosyncratic shocks.

- Competition: Bharat Forge, Ramkrishna Forgings, MM Forgings, and imports limit pricing power in overlapping segments.

Valuation

At a P/E of 69.99x and a market cap of ₹1,765 crore, Amic Forging is priced as if the latest quarter is an aberration and historic margins and growth will return. This is plausible but unverified. The bull case rests on specialty-forgings demand being structurally robust, the 27.89% ROCE pointing to underlying business quality, and the cash-flow turnaround as evidence of operational discipline. If revenue growth returns to 20%+ with margin recovery, the multiple becomes defensible.

The bear case: P/E of 70 with 45% profit decline is unsustainable unless recovery is rapid. PEG analysis is unhelpful with negative profit growth; valuation rests entirely on forward expectations rather than trailing fundamentals. Benchmarked to forgings peers, Amic trades at a meaningful premium to Bharat Forge and RKFL on trailing earnings, justified only by the small-cap growth narrative.

Business Strategy & Outlook

Strategy centres on four areas. First, deepen positioning in specialty open-die forgings for power, oil and gas, defence, and process-industry customers — segments where competition is limited and pricing stronger than commoditised forgings. Second, expand capacity carefully — adding press tonnage, heat-treatment furnaces, and machining capability to take on larger customer programmes.

Third, qualify with high-value customers (power-equipment OEMs, defence prime contractors, oilfield equipment makers) where qualification cycles are long but customer stickiness is high once approved. Fourth, manage working capital and order-execution discipline to translate revenue into cash flow.

The positive cash-flow turnaround in a soft P&L quarter is encouraging. The next watch-items are revenue recovery in subsequent quarters, customer-mix evolution, and any disclosure of capacity additions or large order wins.

Frequently Asked Questions

Q1. What does Amic Forging do?

It manufactures specialty open-die forgings and rolled rings for power generation, oil and gas, defence, cement, steel, and general engineering customers. Open-die forgings are technically demanding, customer-specified components that command premium pricing versus commoditised automotive forgings.

Q2. Why did profit fall 45% on flat revenue?

Operating de-leverage — fixed costs unchanged while revenue growth of only 4.57% was insufficient to cover the cost base, with possible unfavourable product mix, raw-material cost pressure (steel, alloys), and potentially specific inventory or one-off impacts. The disconnect between modest revenue growth and sharp profit drop indicates the business is operating below its optimal utilisation threshold.

Q3. Is the cash-flow turnaround sustainable?

Operating cash flow moved from negative ₹7.96 Cr to positive ₹6.02 Cr — a real improvement indicating better working-capital management. Sustainability depends on revenue and margin recovery; absent a meaningful topline rebound, further improvements are constrained.

Q4. Why is the P/E so high for a small-cap with falling profit?

The market is pricing in a recovery story plus the small-cap premium that often attaches to under-covered specialty-manufacturing names. Risk of multiple compression is real and substantial if recovery is delayed. A stress-test at 30–35x P/E (the RKFL/MM Forgings level) implies 50–60% downside from current levels.

Q5. What are the key risks?

Small-cap liquidity and volatility, customer concentration, valuation risk at 70x P/E with falling profit, operating de-leverage below utilisation threshold, capex-cycle reversal in power/oil/defence end-markets, raw-material volatility (steel, alloys), execution risk on specialty orders, competition from established forgings majors, and small-cap governance considerations.