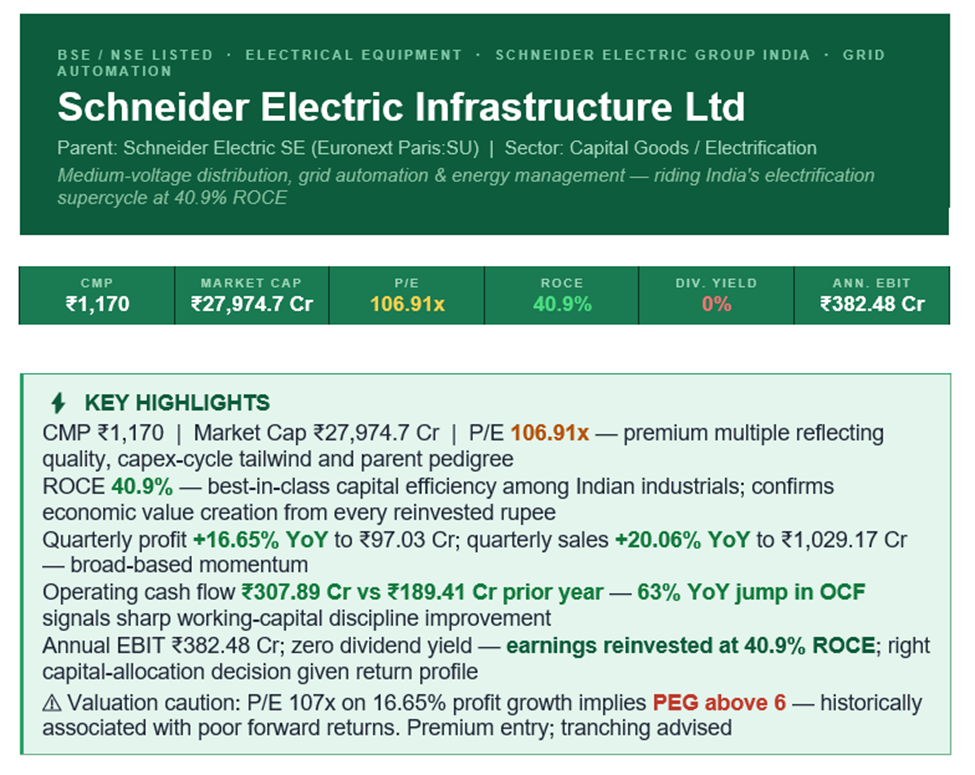

Financials, Valuation & Outlook — Grid Automation & Energy Management Leader at Premium Multiples

Source: company BSE/NSE filings, Schneider Electric group disclosures. Verify current data at bseindia.com and nseindia.com

Company Overview

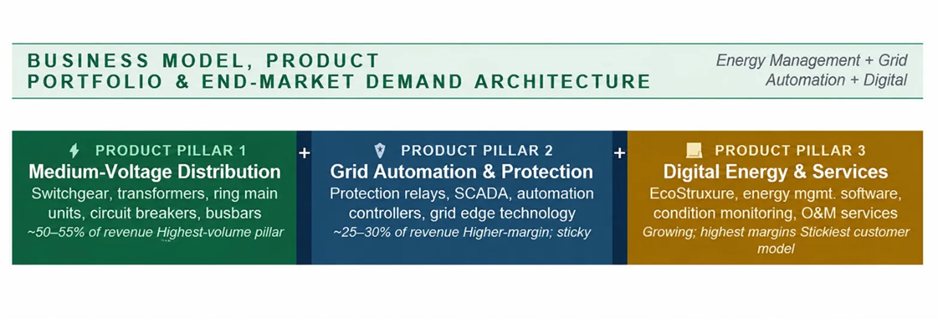

Schneider Electric Infrastructure Limited (NSE/BSE:SCHNEIDER) is the listed Indian arm of the Schneider Electric group — a French multinational (Euronext Paris: SU, market cap ~USD 187 billion) that is one of the world's largest specialists in energy management and digital automation. The Indian listed entity focuses primarily on medium-voltage and low-voltage electrical distribution, grid automation, power transformers, switchgear, and protection relays serving utilities, industrial customers, infrastructure projects, data centres, and increasingly the renewable-energy ecosystem.

Its parent's globally proven product portfolio gives the Indian operation a distinctive edge: it sells technology that has already been engineered for scale, while bringing it to market in one of the world's fastest-growing electrification economies. The parent's R&D spend and global product roadmap continuously replenish the Indian entity's technology offering — a structural advantage that pure domestic peers cannot replicate.

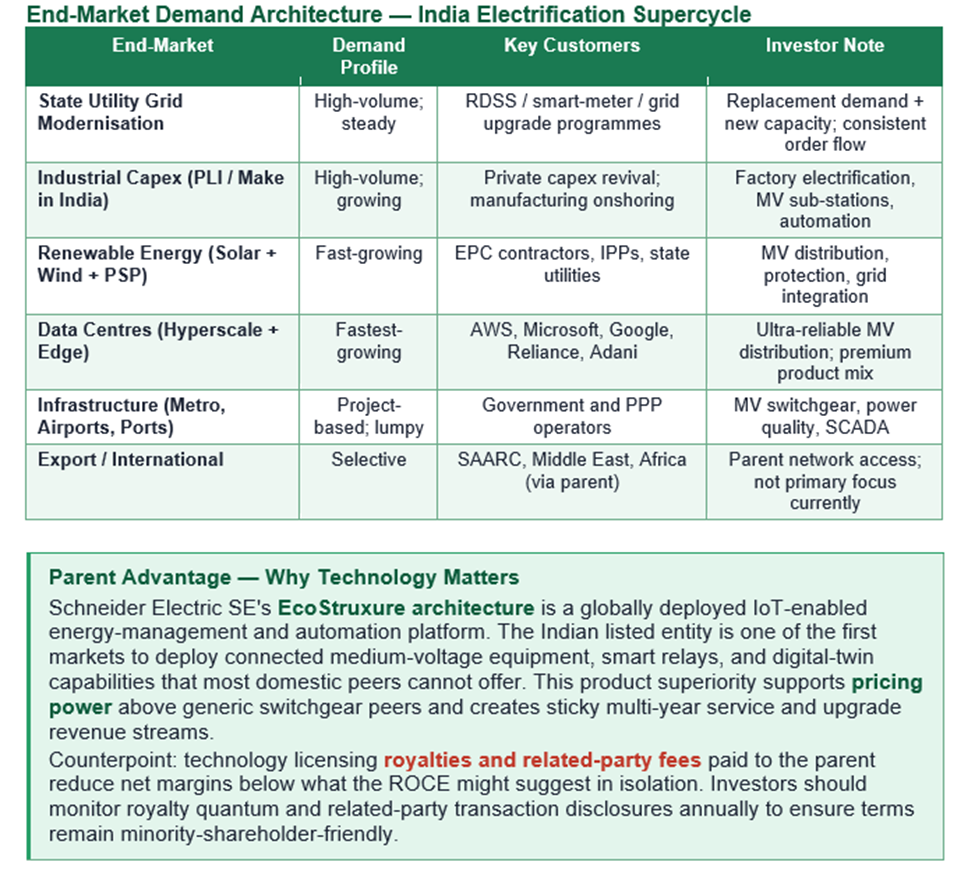

India's structural electrification story is one of the strongest secular themes available to public-market investors today. Power demand is rising on the back of industrial capex revival, manufacturing onshoring under the PLI scheme, the rapid build-out of data centres, and an unprecedented pace of renewable-energy capacity addition. Each of these themes converts directly into demand for medium-voltage equipment, switchgear, protection systems, and grid digitisation — Schneider Electric Infrastructure's core strength. The company also benefits from rising replacement demand as state utilities upgrade decades-old grid infrastructure under government modernisation programmes.

Financial Performance & Insights

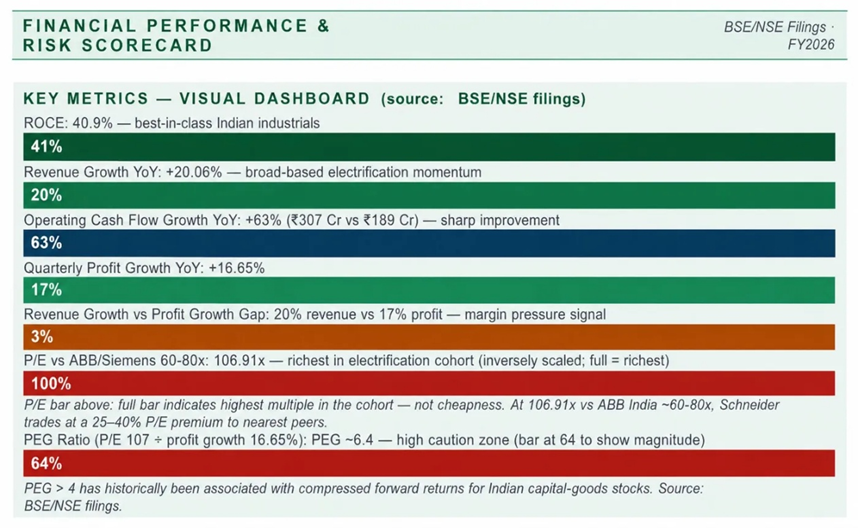

The latest quarter's numbers reinforce the structural growth thesis. Revenue of ₹1,029.17 crore grew 20.06% YoY — a healthy print for a business of this scale operating in long-cycle industrial markets. Net profit of ₹97.03 crore was up 16.65%, slightly trailing top-line growth, indicating margin pressure likely from input costs, project mix, or competitive pricing in particular segments. Annual EBIT of ₹382.48 crore implies an EBIT margin in the high single digits to low double digits, consistent with the global capital-goods norm.

The most striking number in the financials is operating cash flow: ₹307.89 crore versus ₹189.41 crore in the prior year — a 63% YoY jump. For a business with long working-capital cycles and project-based revenue, this kind of cash conversion improvement is a powerful indicator of execution quality. It suggests that receivables collection has improved, advances are being managed better, or both.

ROCE of 40.9% places the company in the very top tier of Indian industrials. Very few capital-goods franchises operate at this level of capital efficiency. The combination of double-digit revenue growth, strong cash conversion, and best-in-class ROCE creates a high-quality earnings stream. The trade-off — discussed in the valuation section — is that the market has fully recognised this quality, and the stock price reflects very high expectations.

Risk ratings are qualitative assessments based on BSE/NSE filings. Conduct independent due diligence.

Price Performance

Capital-goods and electrification names have rerated significantly over the past two to three years as investors appreciated the durability of India's capex cycle. Stocks in this cohort — including ABB India, Siemens, CG Power, and Hitachi Energy — have all delivered substantial returns and now command rich multiples. Schneider Electric Infrastructure has participated in this rerating, and price action tends to track the broader capital-goods index, with idiosyncratic moves around quarterly results, large order announcements, and parent-company strategic updates.

For investors entering at current levels, the price-performance setup demands realism. Most of the easy multiple expansion has already happened. From here, returns are likely to be driven primarily by earnings growth, and the stock will be sensitive to any quarter where order inflows or execution disappoint.

Valuation

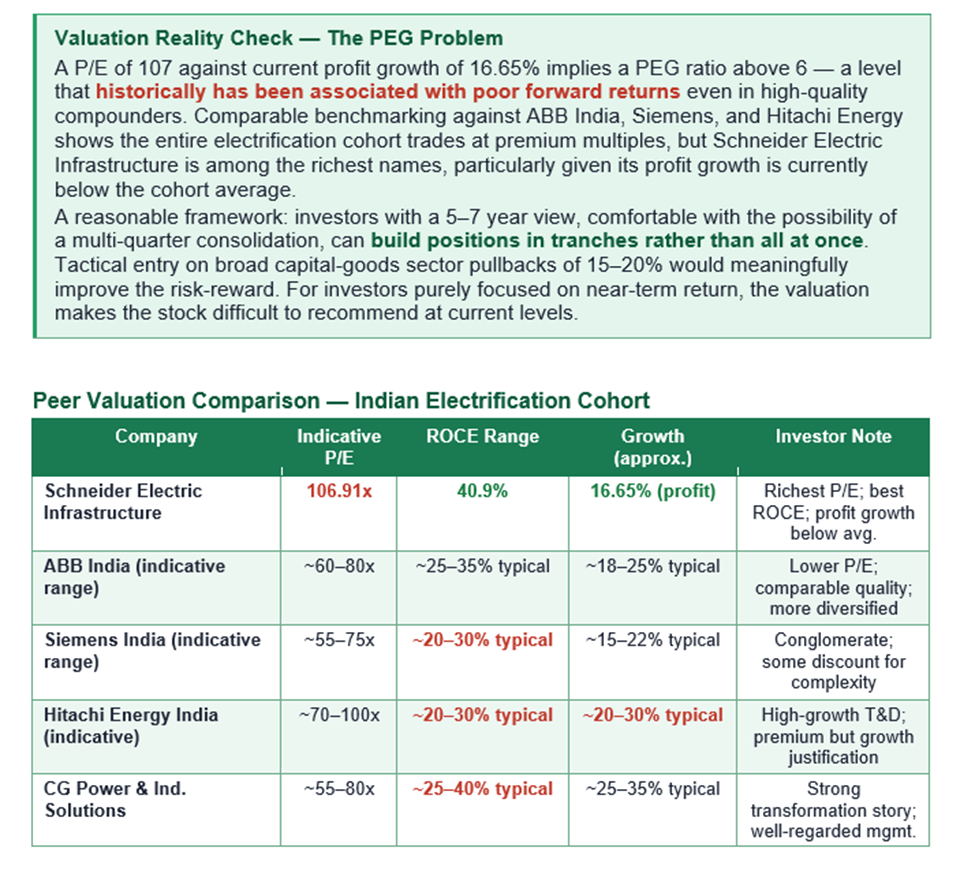

At a trailing P/E of 106.91x and zero dividend yield, Schneider Electric Infrastructure is priced for sustained mid-to-high-teens earnings growth over multiple years. The bull case anchors on three points: India's electrification capex cycle has years to run; the company's 40.9% ROCE earns it a permanent premium over average industrials; and the parent's technology pipeline supports both volume and mix-led margin expansion.

Indicative peer P/E and ROCE ranges sourced from publicly available analyst reports. Not company-specific recommendations. Verify current peer multiples.

Key Risks

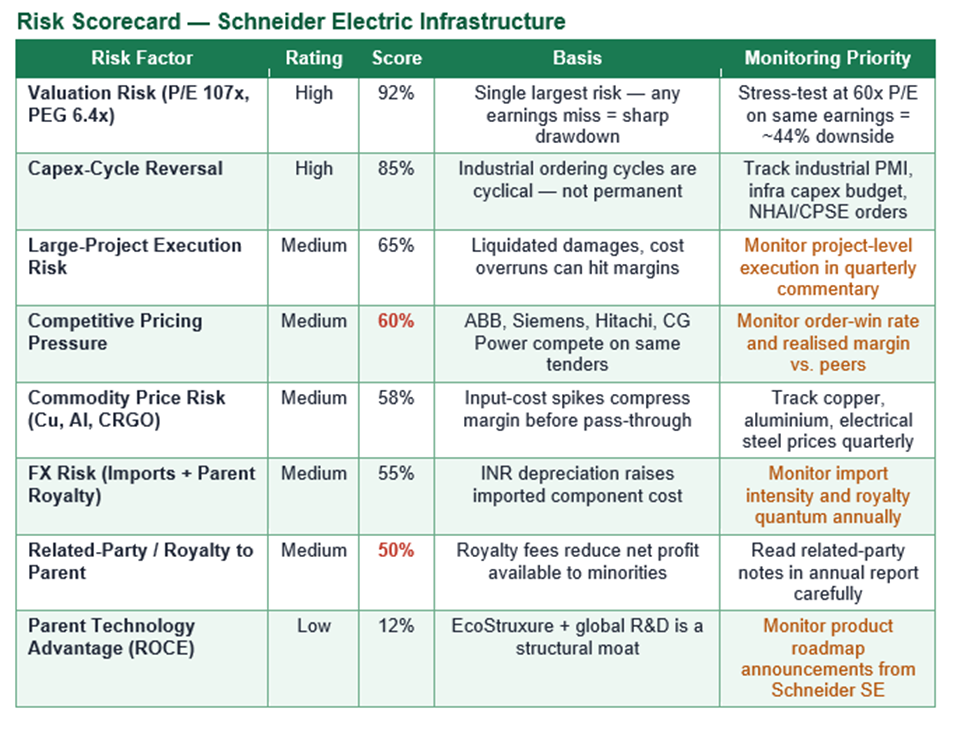

1 — Valuation Risk (Primary)

At P/E 106.91, even modest earnings disappointment can compress the multiple meaningfully and produce drawdowns that wipe out years of returns. The PEG ratio of ~6.4 is historically in the danger zone. Investors should stress-test their position against a scenario where the P/E re-rates to 60x (the level of ABB India) on unchanged earnings — the implied downside would be approximately 44% from current levels.

2 — Capex-Cycle Reversal

While the current Indian capex cycle is robust, it is cyclical by nature. When industrial ordering eventually slows, capital-goods stocks de-rate sharply. Schneider Electric Infrastructure has historically been a cyclical business, and the current premium multiple assumes the cycle will remain favourable for an extended period.

3 — Other Risks

- Execution risk: Large-project delivery delays, cost overruns, and liquidated damages can hit margins materially.

- Competitive pressure: ABB, Siemens, Hitachi Energy, CG Power, and domestic players compete on the same tenders; pricing discipline can erode.

- Commodity risk: Copper, aluminium, and CRGO electrical steel are major cost inputs. Sustained spikes compress margins until prices pass through.

- Foreign exchange risk: Imported components and royalty payments to the parent expose net margins to INR depreciation.

- Related-party transactions: Royalty, technology fees, and related sales/purchases with the parent warrant ongoing investor scrutiny on terms and quantum.

Business Strategy & Outlook

The strategic playbook centres on four pillars. First, riding the medium-voltage and grid-automation upgrade cycle as state utilities and private industrial customers modernise infrastructure. Second, capturing share of the data-centre electrification opportunity, where demand for reliable medium-voltage distribution is exploding alongside hyperscaler investment in India.

Third, leveraging the parent's global product roadmap to introduce digital and software-enabled offerings — energy management software, condition monitoring, predictive maintenance — that command higher margins and create stickier customer relationships. Fourth, deepening manufacturing localisation to qualify for public-sector tenders and benefit from PLI-style incentives.

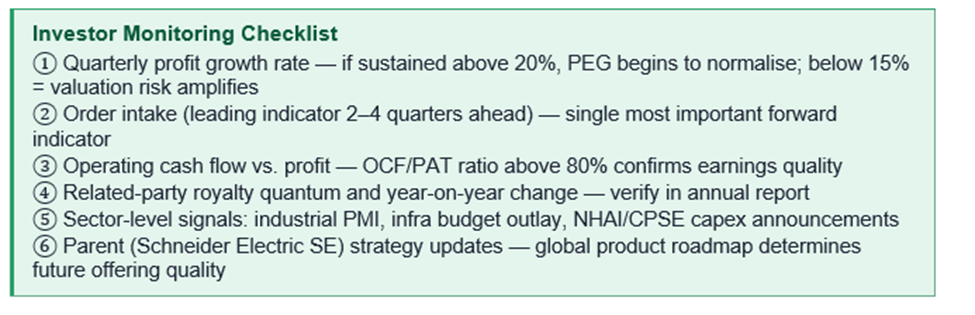

The sharp jump in operating cash flow alongside double-digit revenue growth suggests management is executing well on order-book conversion and working-capital discipline. The next watch-items are order intake (a leading indicator of growth two to four quarters out), product-mix shift towards software and services, and sustained ROCE leadership.

Frequently Asked Questions

Q1. What does Schneider Electric Infrastructure do?

It is the Indian listed subsidiary of the Schneider Electric group, focused on medium-voltage and low-voltage electrical distribution, grid automation, transformers, switchgear, and energy-management products serving utilities, industrials, infrastructure, data centres, and renewables.

Q2. Why does Schneider Electric Infrastructure trade at a P/E of 107x?

The market is pricing in a long runway of capex-cycle-driven growth, best-in-class 40.9% ROCE, and the parent's technology pipeline. The flip side is significant valuation risk — a PEG of ~6.4 implies the market is pricing in rapid sustained growth. Any disappointment risks a sharp de-rating.

Q3. Does the company pay dividends?

No. Dividend yield is 0%. Earnings are being reinvested, supported by very high ROCE. For a business compounding at 40.9% ROCE, retaining earnings is the economically rational choice — provided reinvestment opportunities continue at this return level.

Q4. How does Schneider Electric Infrastructure compare with ABB and Siemens?

All three operate in overlapping segments and trade at premium multiples. Schneider Electric Infrastructure has higher ROCE than peers but currently slightly lower revenue growth than the cohort average. Its P/E is among the richest in the peer set.

Q5. What are the biggest risks?

Valuation risk at 107x P/E (PEG ~6.4), capex-cycle reversal, large-project execution slippage, competitive pricing pressure, commodity-price spikes (copper, aluminium, CRGO), FX exposure on imports and parent royalty, and related-party transaction quantum. Valuation risk is the dominant near-term concern.

Q6. Is Schneider Electric Infrastructure a good buy at current levels?

For long-term (5–7 year) investors comfortable with significant near-term volatility, the quality of the franchise and structural demand tailwind is compelling. For shorter-horizon investors, the P/E 107x / PEG 6.4x combination makes the risk-reward difficult to justify without a meaningful price correction. Tranching into positions on sector-wide pullbacks of 15–20% would improve the setup.